Navigate

Article List

- The Gold Principles: Building Responsible Progress Across the Gold Value Chain

By ALBERT CHENG, Chair, Gold Principles Group; CEO, Singapore Bullion Market Association

- OPINION - INDONESIA’S BULLION MARKET TRANSFORMATION: ATM GOLD AND INNOVATION DRIVING THE NEXT GROWTH PHASE

By DAVID MAKSUD, President Director, Brink’s Indonesia

- Digital Gold in Southeast Asia

By TAN KWAY GUAN, Central Banks and Public Policy Lead (Singapore), World Gold Council

- The growth of Derivatives and the Case for Regional Metals Markets

By RUSSELL ROBERTSON, Chief Business Development Officer, Abaxx Exchange and Clearing

- Why tokenisation Matters for the Bullion Industry and How Carrying Costs Fit In

By EVA MENG, Head of Matrixdock

- Dubai’s Bullion Hub Comes of Age: DBRG and the Next Chapter for the UAE

By MOHAMMAD AYYOB, Chairman, Dubai Business Group for Bullion and Gold Refinery (DBRG)

- SBMA News

By SBMA

Article List

- The Gold Principles: Building Responsible Progress Across the Gold Value Chain

By ALBERT CHENG, Chair, Gold Principles Group; CEO, Singapore Bullion Market Association

- OPINION - INDONESIA’S BULLION MARKET TRANSFORMATION: ATM GOLD AND INNOVATION DRIVING THE NEXT GROWTH PHASE

By DAVID MAKSUD, President Director, Brink’s Indonesia

- Digital Gold in Southeast Asia

By TAN KWAY GUAN, Central Banks and Public Policy Lead (Singapore), World Gold Council

- The growth of Derivatives and the Case for Regional Metals Markets

By RUSSELL ROBERTSON, Chief Business Development Officer, Abaxx Exchange and Clearing

- Why tokenisation Matters for the Bullion Industry and How Carrying Costs Fit In

By EVA MENG, Head of Matrixdock

- Dubai’s Bullion Hub Comes of Age: DBRG and the Next Chapter for the UAE

By MOHAMMAD AYYOB, Chairman, Dubai Business Group for Bullion and Gold Refinery (DBRG)

- SBMA News

By SBMA

The growth of Derivatives and the Case for Regional Metals Markets

By RUSSELL ROBERTSON, Chief Business Development Officer, Abaxx Exchange and Clearing

The History of Derivatives

the origins of futures trading can be tracked back to 1634 with the dutch “tulip mania”

Supply and Demand Fundamentals

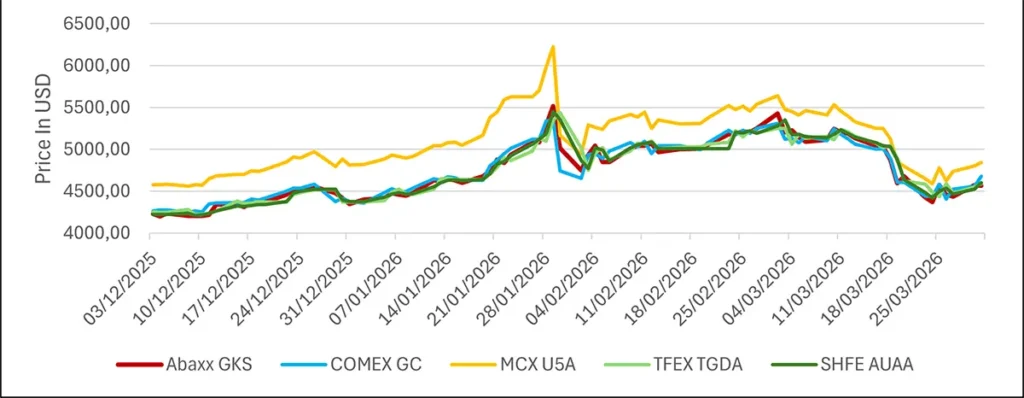

Price Correlation and Regional Focus

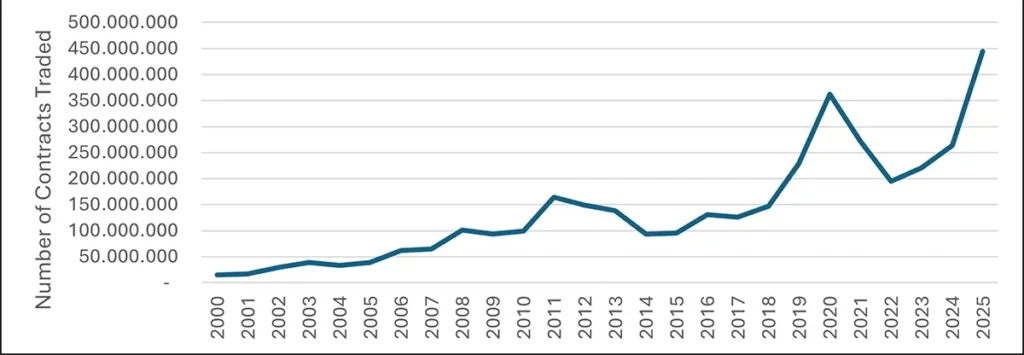

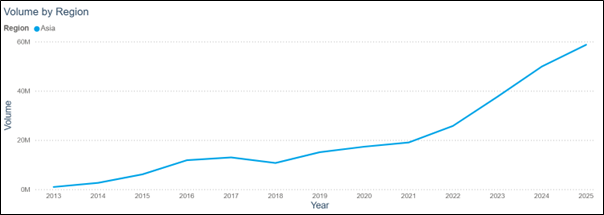

Gold Futures Contracts Traded per Year

As participation in precious metals markets grows and price volatility persists, the case for regional trading hubs and localised price discovery becomes compelling. There is a clear need to capture the price of gold at its point of consumption – not just at financial hubs such as London and New York, where the physical bars in question may never have traded.

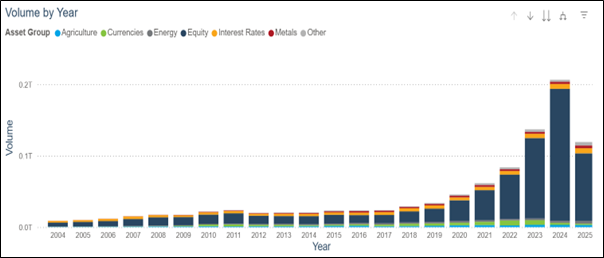

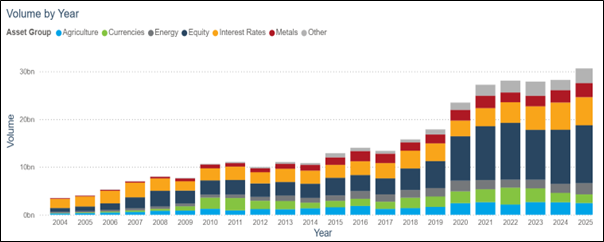

Gold Derivatives Portfolio End of Day Settlments

As the geopolitical landscape shifts and attention turns increasingly to regional commodity pricing, FIA data confirms significant volume growth in Asia-based metals trading.

Conclusion