Navigate

Article List

- The Gold Principles: Building Responsible Progress Across the Gold Value Chain

By ALBERT CHENG, Chair, Gold Principles Group; CEO, Singapore Bullion Market Association

- OPINION - INDONESIA’S BULLION MARKET TRANSFORMATION: ATM GOLD AND INNOVATION DRIVING THE NEXT GROWTH PHASE

By DAVID MAKSUD, President Director, Brink’s Indonesia

- Digital Gold in Southeast Asia

By TAN KWAY GUAN, Central Banks and Public Policy Lead (Singapore), World Gold Council

- The growth of Derivatives and the Case for Regional Metals Markets

By RUSSELL ROBERTSON, Chief Business Development Officer, Abaxx Exchange and Clearing

- Why tokenisation Matters for the Bullion Industry and How Carrying Costs Fit In

By EVA MENG, Head of Matrixdock

- Dubai’s Bullion Hub Comes of Age: DBRG and the Next Chapter for the UAE

By MOHAMMAD AYYOB, Chairman, Dubai Business Group for Bullion and Gold Refinery (DBRG)

- SBMA News

By SBMA

Article List

- The Gold Principles: Building Responsible Progress Across the Gold Value Chain

By ALBERT CHENG, Chair, Gold Principles Group; CEO, Singapore Bullion Market Association

- OPINION - INDONESIA’S BULLION MARKET TRANSFORMATION: ATM GOLD AND INNOVATION DRIVING THE NEXT GROWTH PHASE

By DAVID MAKSUD, President Director, Brink’s Indonesia

- Digital Gold in Southeast Asia

By TAN KWAY GUAN, Central Banks and Public Policy Lead (Singapore), World Gold Council

- The growth of Derivatives and the Case for Regional Metals Markets

By RUSSELL ROBERTSON, Chief Business Development Officer, Abaxx Exchange and Clearing

- Why tokenisation Matters for the Bullion Industry and How Carrying Costs Fit In

By EVA MENG, Head of Matrixdock

- Dubai’s Bullion Hub Comes of Age: DBRG and the Next Chapter for the UAE

By MOHAMMAD AYYOB, Chairman, Dubai Business Group for Bullion and Gold Refinery (DBRG)

- SBMA News

By SBMA

DIGITAL GOLD IN SOUTHEAST ASIA

By TAN KWAY GUAN, Central Banks and Public Policy Lead (Singapore), World Gold Council

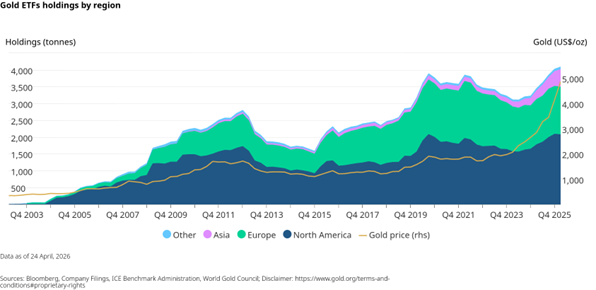

Gold ETFs Holdings by Region

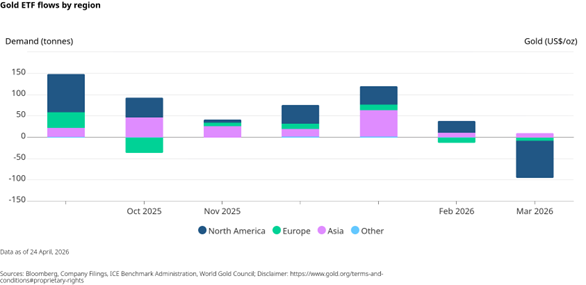

Gold ETFs Flows by Region

- Making it easy to start and continue investing (e.g., small minimums, recurring buys, simple portfolio placement).

- Offering the right format for different needs (e.g., ETF-like exposure, vaulted accounts, tokenised products).

- Building confidence with clear pricing, clear custody and audit information, and simple rules for selling or taking delivery.

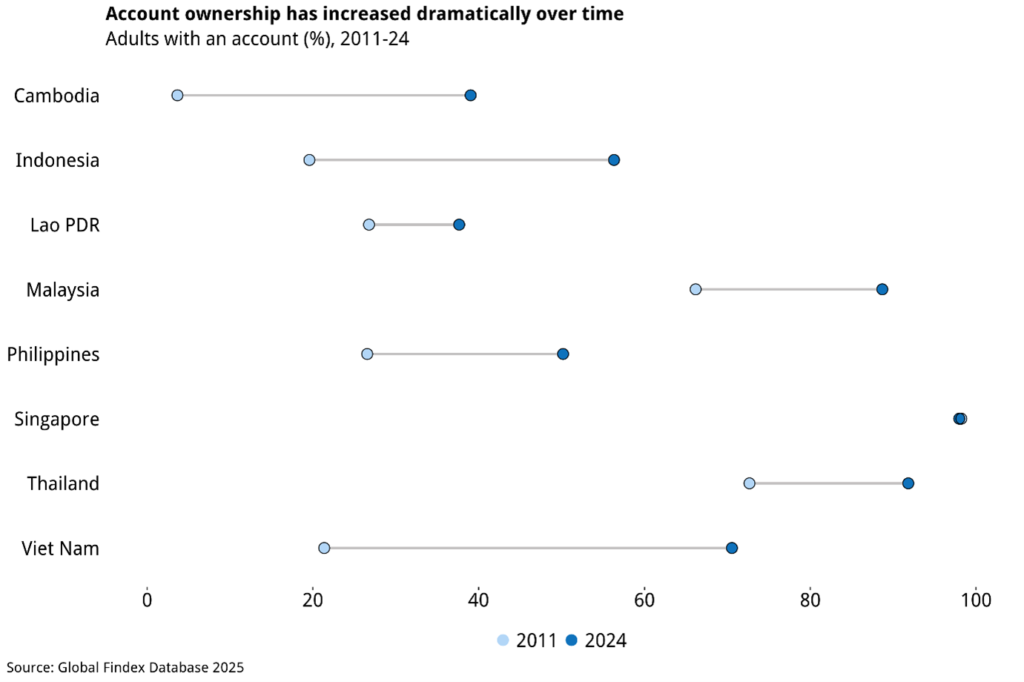

South east Asia’s Market Potential

Account Ownership Has Increassed Dramatically Over Time Adult With an Account (%), 2011-24

Potential Challenges