Navigate

Article List

- The Gold Principles: Building Responsible Progress Across the Gold Value Chain

By ALBERT CHENG, Chair, Gold Principles Group; CEO, Singapore Bullion Market Association

- OPINION - INDONESIA’S BULLION MARKET TRANSFORMATION: ATM GOLD AND INNOVATION DRIVING THE NEXT GROWTH PHASE

By DAVID MAKSUD, President Director, Brink’s Indonesia

- Digital Gold in Southeast Asia

By TAN KWAY GUAN, Central Banks and Public Policy Lead (Singapore), World Gold Council

- The growth of Derivatives and the Case for Regional Metals Markets

By RUSSELL ROBERTSON, Chief Business Development Officer, Abaxx Exchange and Clearing

- Why tokenisation Matters for the Bullion Industry and How Carrying Costs Fit In

By EVA MENG, Head of Matrixdock

- Dubai’s Bullion Hub Comes of Age: DBRG and the Next Chapter for the UAE

By MOHAMMAD AYYOB, Chairman, Dubai Business Group for Bullion and Gold Refinery (DBRG)

- SBMA News

By SBMA

Article List

- The Gold Principles: Building Responsible Progress Across the Gold Value Chain

By ALBERT CHENG, Chair, Gold Principles Group; CEO, Singapore Bullion Market Association

- OPINION - INDONESIA’S BULLION MARKET TRANSFORMATION: ATM GOLD AND INNOVATION DRIVING THE NEXT GROWTH PHASE

By DAVID MAKSUD, President Director, Brink’s Indonesia

- Digital Gold in Southeast Asia

By TAN KWAY GUAN, Central Banks and Public Policy Lead (Singapore), World Gold Council

- The growth of Derivatives and the Case for Regional Metals Markets

By RUSSELL ROBERTSON, Chief Business Development Officer, Abaxx Exchange and Clearing

- Why tokenisation Matters for the Bullion Industry and How Carrying Costs Fit In

By EVA MENG, Head of Matrixdock

- Dubai’s Bullion Hub Comes of Age: DBRG and the Next Chapter for the UAE

By MOHAMMAD AYYOB, Chairman, Dubai Business Group for Bullion and Gold Refinery (DBRG)

- SBMA News

By SBMA

Why tokenisation Matters for the Bullion Industry and How Carrying Costs Fit In

By EVA MENG, Head of Matrixdock

What ETFs Did and What Tokens Can Do Next

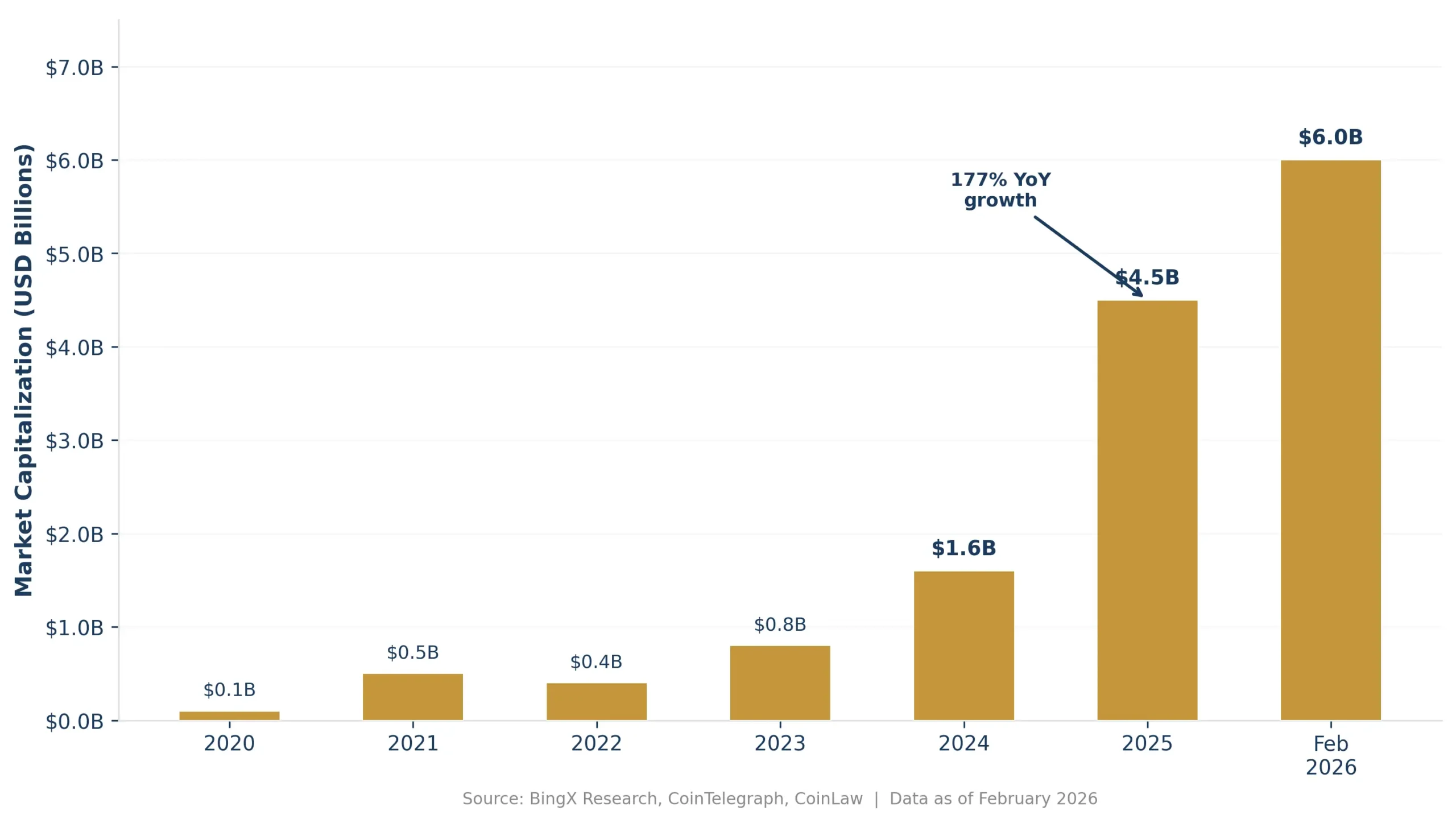

Tokenised Gold: Market Cap Growth

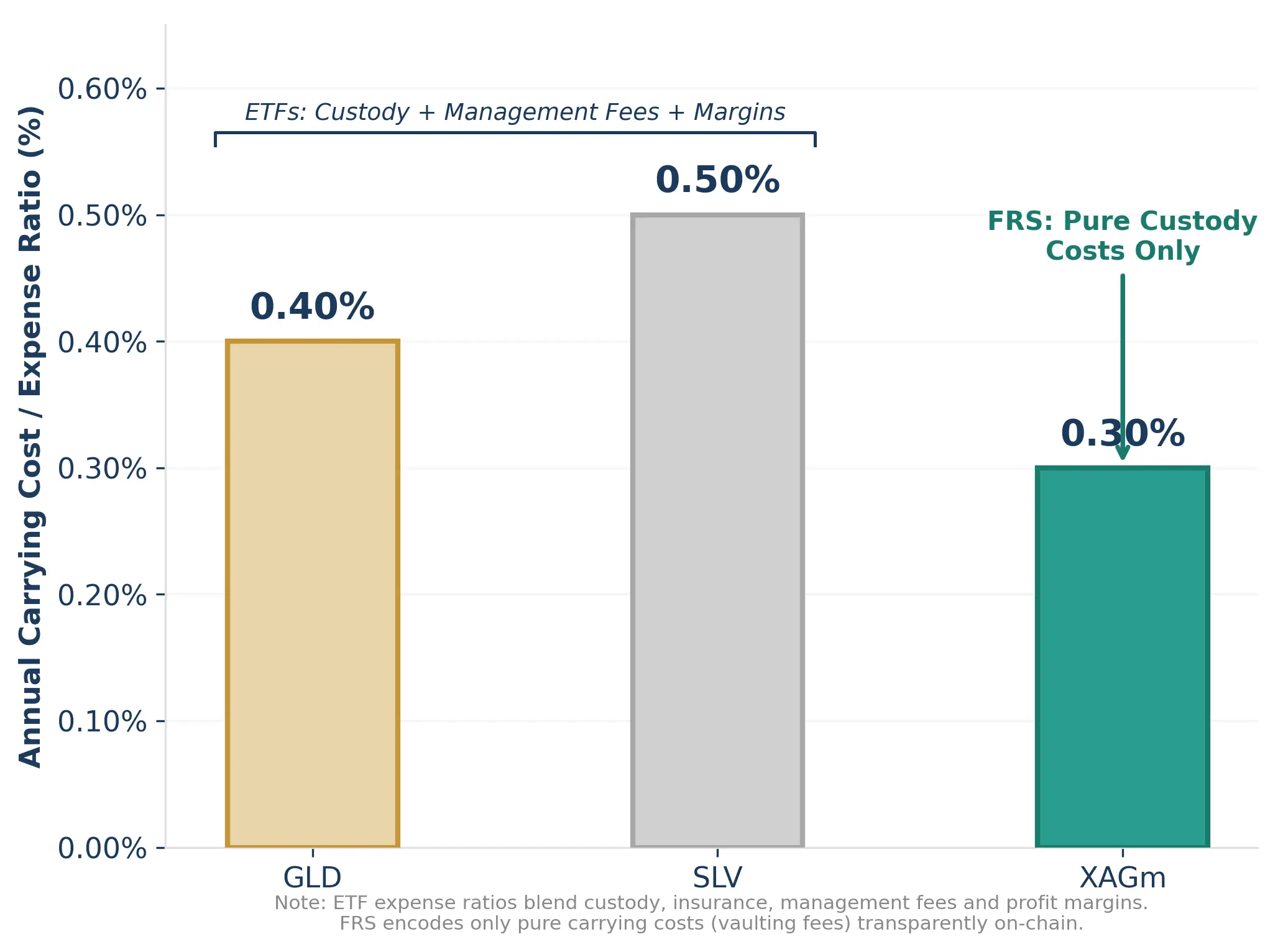

The Carrying Cost Challenge and a Silver Solution

Carrying Costs:

Precious Metal ETFs vs.

FRS-Based Tokens

The framework is built on what it calls the Economic Purity Principle: the token must faithfully represent the underlying asset’s economic characteristics, including its negative carry, rather than masking or transforming them. FRS preserves full compatibility with digital financial markets, where tokens built on it are designed to function in lending, trading, and collateral applications without requiring wrappers or rebasing that fragmented liquidity. It is asset-agnostic: applicable to any physical asset with predictable holding costs, from silver to platinum to warehoused commodities.

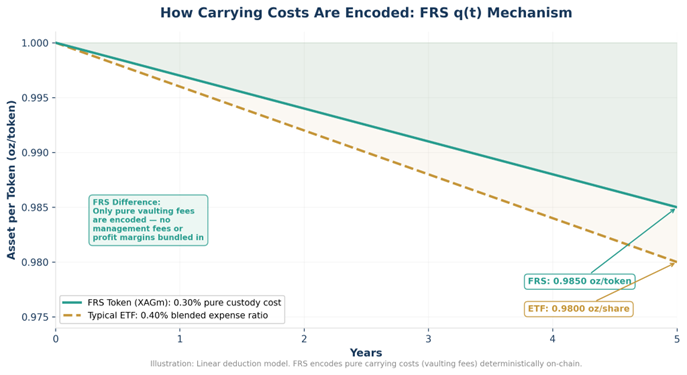

How Carrying Costs Are Encoded: FRS q(t) Mechanism)

From Theory to Practice

The Road Ahead

This article is brought to you by SBMA in association with Matrixdock.