Navigate

Article List

- Strategic Expansion & Market Adaptation: YLG Bullion’s Journey Into Dubai’s Gold Arena

By Pawan Nawawattanasub, CEO, YLG Bullion International

- HISTORY OF GOLD IN AUSTRALIA & FUTURE TRENDS

By Nicholas Frappell, Global Head Institutional Markets, ABC Refinery

- KIS GOLD PRICES PLAYING CRUCIAL ROLE IN DEVELOPMENT OF ASIA GOLD HUB

By Kallanish Index Services

- THE WORLD GOLD COUNCIL’S VISION FOR THE GOLD MARKET

By Chen Qinghan, Central Banks and Public Policy Lead, World Gold Council

- LAOS’ GOLD RUSH: A GOLDEN OPPORTUNITY FOR ECONOMIC GROWTH

By PTL Holding Company Limited

- US ELECTION DYNAMICS A POSITIVE FOR GOLD, WITH MIXED IMPACT ON KEY COMMODITIES

By Bart Melek, Managing Director & Global Head of Commodity Strategy, TD Securities

- BUILDING ASIAN BULLION TIGERS

By FINMET PTE LTD

- The ASEAN Gold Market – A 2024 Update

By Nikos Kavalis, Managing Director, Metals Focus Singapore Pte Ltd

- LBMA & SBMA: A Golden Partnership

By Ruth Crowell, Chief Executive, LBMA

- SBMA News

By SBMA

Article List

- Strategic Expansion & Market Adaptation: YLG Bullion’s Journey Into Dubai’s Gold Arena

By Pawan Nawawattanasub, CEO, YLG Bullion International

- HISTORY OF GOLD IN AUSTRALIA & FUTURE TRENDS

By Nicholas Frappell, Global Head Institutional Markets, ABC Refinery

- KIS GOLD PRICES PLAYING CRUCIAL ROLE IN DEVELOPMENT OF ASIA GOLD HUB

By Kallanish Index Services

- THE WORLD GOLD COUNCIL’S VISION FOR THE GOLD MARKET

By Chen Qinghan, Central Banks and Public Policy Lead, World Gold Council

- LAOS’ GOLD RUSH: A GOLDEN OPPORTUNITY FOR ECONOMIC GROWTH

By PTL Holding Company Limited

- US ELECTION DYNAMICS A POSITIVE FOR GOLD, WITH MIXED IMPACT ON KEY COMMODITIES

By Bart Melek, Managing Director & Global Head of Commodity Strategy, TD Securities

- BUILDING ASIAN BULLION TIGERS

By FINMET PTE LTD

- The ASEAN Gold Market – A 2024 Update

By Nikos Kavalis, Managing Director, Metals Focus Singapore Pte Ltd

- LBMA & SBMA: A Golden Partnership

By Ruth Crowell, Chief Executive, LBMA

- SBMA News

By SBMA

THE ASEAN GOLD MARKET – A 2024 UPDATE

By Nikos Kavalis, Managing Director, Metals Focus Singapore Pte Ltd

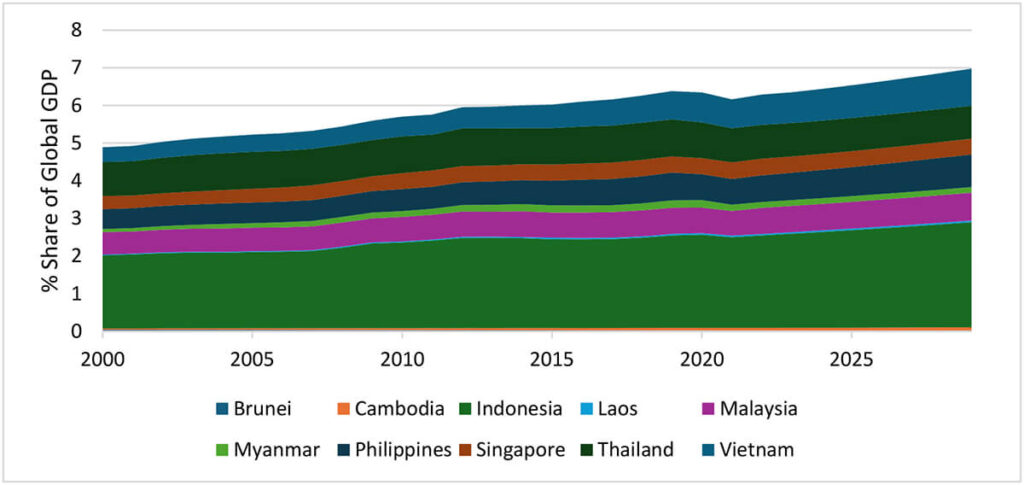

A GROUP OF VIBRANT AND GROWING ECONOMIES

ASEAN Countries’ Share of Global GDP, History & Forecast*

Source: IMF World Economic Outlook, April 2024

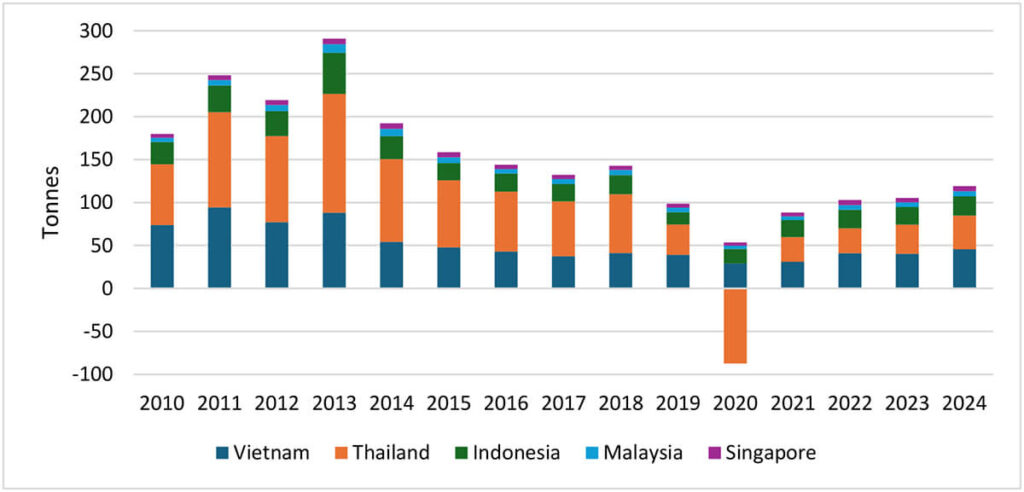

HOME TO KEY MID-TIER GOLD MARKETS AND A TRADING HUB

Key ASEAN Countries Net Retail Investment Demand

STRUCTURAL CHANGES TO GOLD INDUSTRY AN OPPORTUNITY FOR ASEAN

Key ASEAN Countries Jewellery Fabrication

Share of Bullion Exports Shipped to ASEAN Countries*

Source: Thai Customs Department, Statistics Indonesia, Metals Focus