PLATINUM CORNER

Platinum Perspectives

Latest Update

2 April 2026

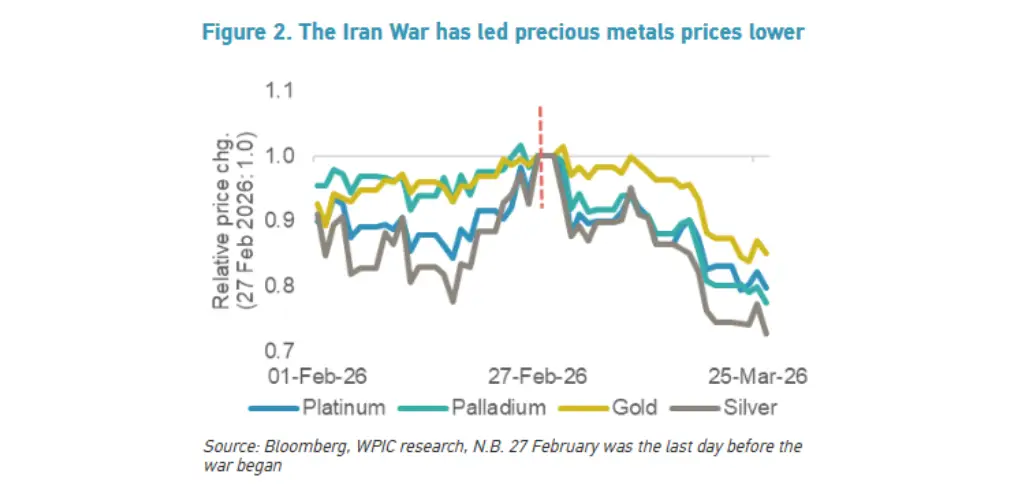

The Iran War’s direct impact on platinum demand appears modest, but higher interest rate expectations and a stronger US dollar could weigh on investment demand

The Iran war has entered its second month. Iran and the broader Middle East (ME) are not large direct markets for platinum supply and demand. Contagion impacts currently appear more likely from the economic drag caused by restrictions across the Strait of Hormuz and the potential for a global helium shortage to impact semiconductor production (which may impact vehicle production).