Navigate

Article List

- China’s VAT Reform and Its Implications for the Gold Market

By RAY JIA, Head of Research (Asia Pacific, ex-India) and Deputy Head of Trade Engagement (China), World Gold Council

- Platinum Group Metals: A New Era for China

By WEIBIN DENG, Regional Head of Asia Pacific, World Platinum Investment Council

- India’s Precious Metals Reset in 2025: Policy Alignment, Market Structure and the Consolidation of Trust

By SRINIVASA MOORTHY & PRATHIK TAMBRE, Research Desk, Bullion World

- Vietnam Charts Path Toward National Gold Exchange: Regional Experts Contribute to Policy Development

By HUYNH TRUNG KHANH, Vice-Chairman, Vietnam Gold Trading Association

- Developing Talent, Sharing Experiences — The Gold Industry Training Programme

By TAN KWAY GUAN, Central Banks and Public Policy Lead (Singapore), World Gold Council

- Regulatory and Policy Shifts in Asia’s Key Bullion Hubs

By LEE LIANG LE, Analyst, Kallanish Index Services

- SBMA News

By SBMA

Article List

- China’s VAT Reform and Its Implications for the Gold Market

By RAY JIA, Head of Research (Asia Pacific, ex-India) and Deputy Head of Trade Engagement (China), World Gold Council

- Platinum Group Metals: A New Era for China

By WEIBIN DENG, Regional Head of Asia Pacific, World Platinum Investment Council

- India’s Precious Metals Reset in 2025: Policy Alignment, Market Structure and the Consolidation of Trust

By SRINIVASA MOORTHY & PRATHIK TAMBRE, Research Desk, Bullion World

- Vietnam Charts Path Toward National Gold Exchange: Regional Experts Contribute to Policy Development

By HUYNH TRUNG KHANH, Vice-Chairman, Vietnam Gold Trading Association

- Developing Talent, Sharing Experiences — The Gold Industry Training Programme

By TAN KWAY GUAN, Central Banks and Public Policy Lead (Singapore), World Gold Council

- Regulatory and Policy Shifts in Asia’s Key Bullion Hubs

By LEE LIANG LE, Analyst, Kallanish Index Services

- SBMA News

By SBMA

Platinum Group Metals: A New Era for China

By WEIBIN DENG, Regional Head of Asia Pacific, World Platinum Investment Council

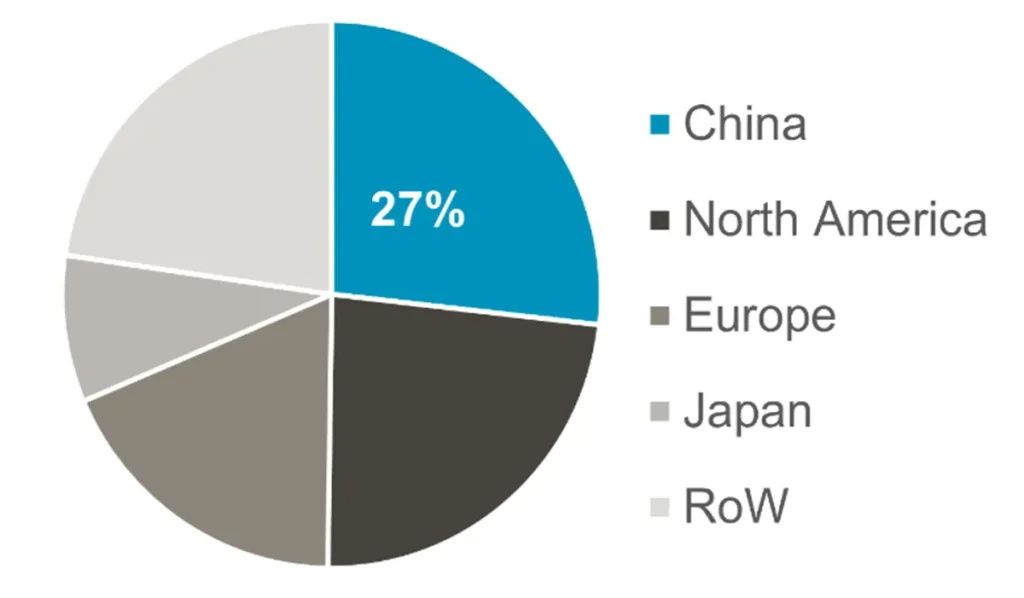

China Leads Global Platinum Demand

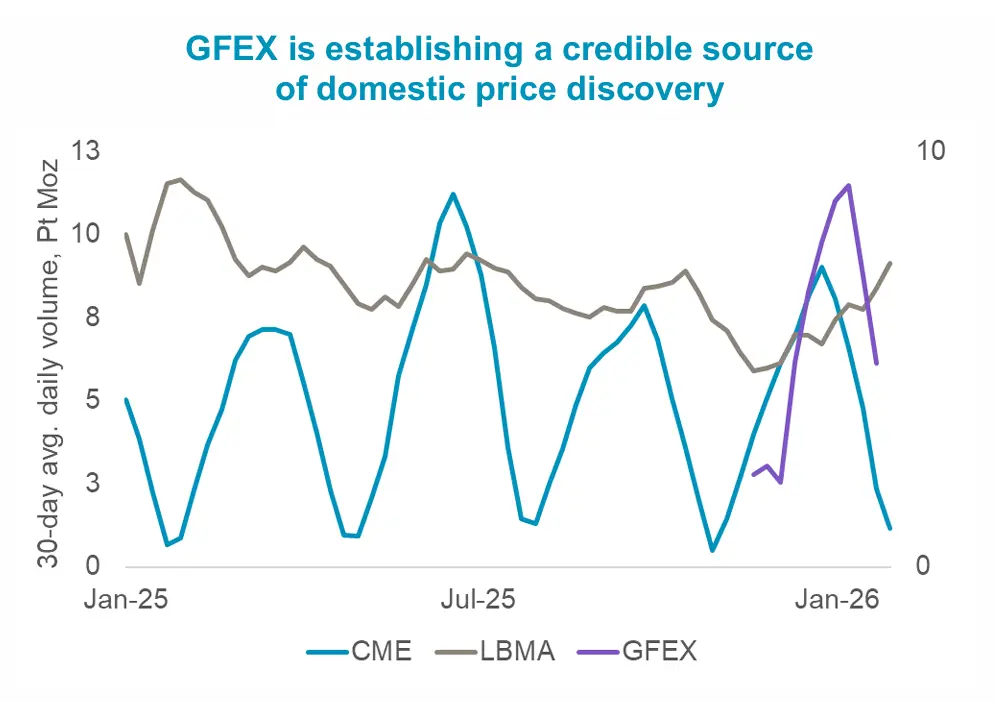

GFEX’s launch of platinum and palladium contracts

Platinum and palladium contracts do not currently have Qualified Foreign Institutional Investor (QFII) status.

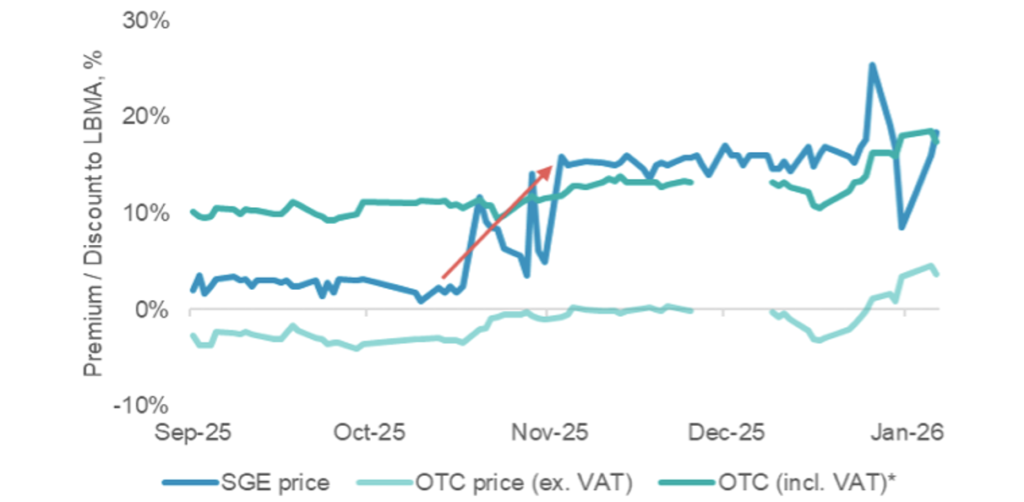

VAT policy change

Chinese platinum demand has historically been price sensitive and is likely to soften on higher costs, potentially dampening short-term demand whilst consumers normalise to new price levels that include VAT.

The Removal of the VAT Exemption on SGE Platinum Sales From 1 November 2025 Caused SGE Prices to Broadly Align With OTC Prices

Impact on recycling

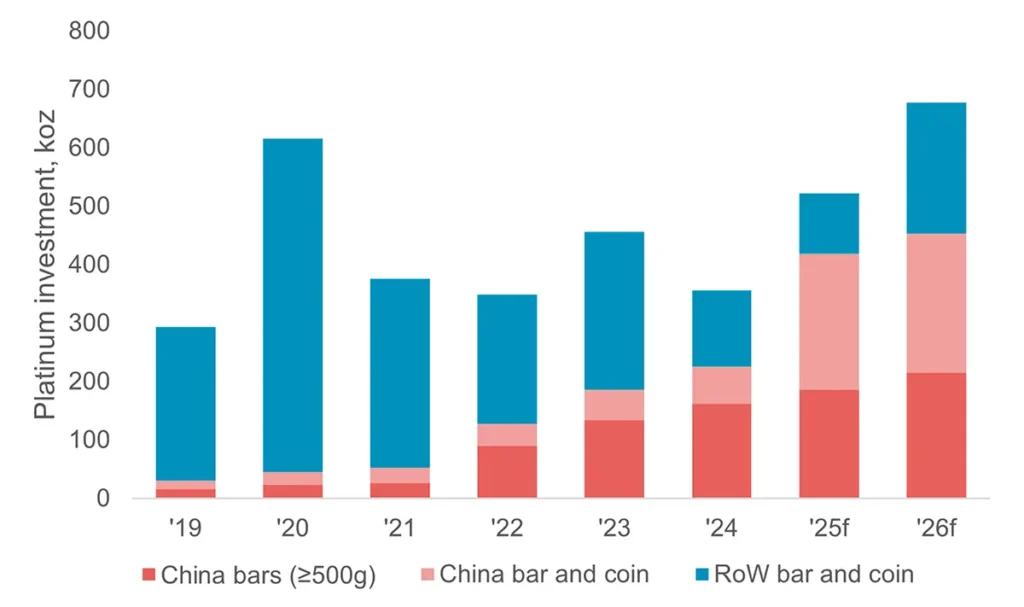

Bar and coin investment demand growth

China Has Grown to Become the Largest Single Market for Platinum Bar and Coin Investment Demand