Navigate

Article List

- Hot Topics Under the Microscope at LBMA/LPPM Global Precious Metals Conference

By Shelly Ford, Digital Content Manager & Editor of the Alchemist, LBMA

- Recent Portfolio Application of Gold ETFs

By Geoff Howie, Market Strategist, Singapore Exchange Limited

- The Digital Transformation of Precious Metal Supply Chains

By Philipp Stockinger, Business Development Engineer, aXedras Group AG

- World Gold Council Singapore – 2022 In Review

By Andrew Naylor, Regional CEO, APAC (ex China) and Public Policy, World Gold Council

- The Next Generation of Tokenised Commodities

By Paul Kelley, Sales & Partnerships, Trovio

- Robust Gold Yields in the Cards

By Bart Melek, Global Head of Commodity Strategy, TD Securities

- Where Beach Meets Bullion

By Strategic Wealth Preservation

- SBMA News

By SBMA

Article List

- Hot Topics Under the Microscope at LBMA/LPPM Global Precious Metals Conference

By Shelly Ford, Digital Content Manager & Editor of the Alchemist, LBMA

- Recent Portfolio Application of Gold ETFs

By Geoff Howie, Market Strategist, Singapore Exchange Limited

- The Digital Transformation of Precious Metal Supply Chains

By Philipp Stockinger, Business Development Engineer, aXedras Group AG

- World Gold Council Singapore – 2022 In Review

By Andrew Naylor, Regional CEO, APAC (ex China) and Public Policy, World Gold Council

- The Next Generation of Tokenised Commodities

By Paul Kelley, Sales & Partnerships, Trovio

- Robust Gold Yields in the Cards

By Bart Melek, Global Head of Commodity Strategy, TD Securities

- Where Beach Meets Bullion

By Strategic Wealth Preservation

- SBMA News

By SBMA

Robust Gold Yields in the Cards

By Bart Melek, Global Head of Commodity Strategy, TD Securities

BART MELEK has over 20 years’ experience analysing precious metals, base metals, energy, financial markets, as well as key economies. He has worked closely with commodity, equity and FX trading desks around the world, and has several forecasting distinctions and top global rankings. Bart contributes to the TD Securities strategic view on commodity, various other markets and macroeconomics. Bart is also a sought-after media commentator. Previous to joining TD, he had senior roles in equities, commodities and risk. He holds a master’s degree in economics from York University in Toronto, with an International Finance/Banking Specialization.

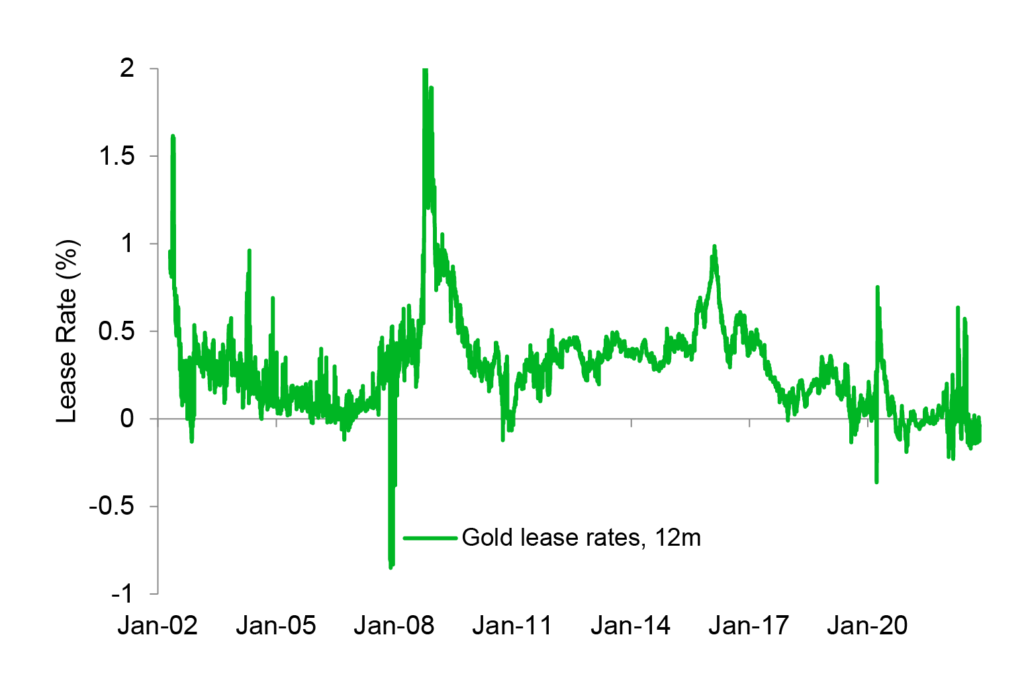

After over a decade scraping the bottom, 12-month gold lease rates have moved distinctively higher to trend above 50 bps, as US monetary policy started to tighten aggressively.

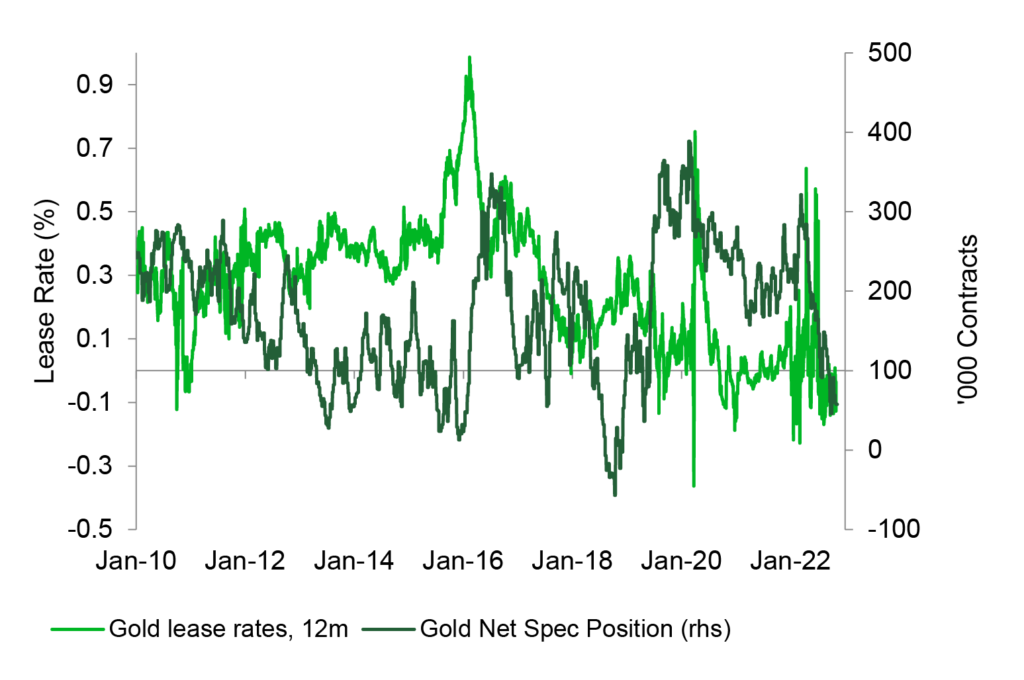

With the Fed continuing to take rates higher in the face of sky-high inflation, real interest rates will continue to rise at an accelerated rate across much of the short end of the Treasury curve. With that, speculative long activity will wane amid higher carry and rising opportunity costs. This implies that gold yields should reach multi-decade highs into 2023.

The widespread view that gold does not offer a yield is a misconception. While income generation from gold is generally not available to most private investors, central banks can actively manage their holdings to deliver returns. This can happen in two major ways: (a) bullion reserves can be lent out to earn the gold deposit rate, or (b) the metal can be swapped for dollars at the gold offered forward rate (GOFO) or the swap rate.

While central banks are also likely to capitalise on the higher gold yield environment by making gold available to the market, they are unlikely to reduce holdings. Gold reserves offer the benefit of being highly liquid holdings, which possess both pro and counter cyclical properties, are a well-recognised store of value for many millennia and are considered strategic assets which are no one’s liability. Physical holdings are also impervious to sanctions.

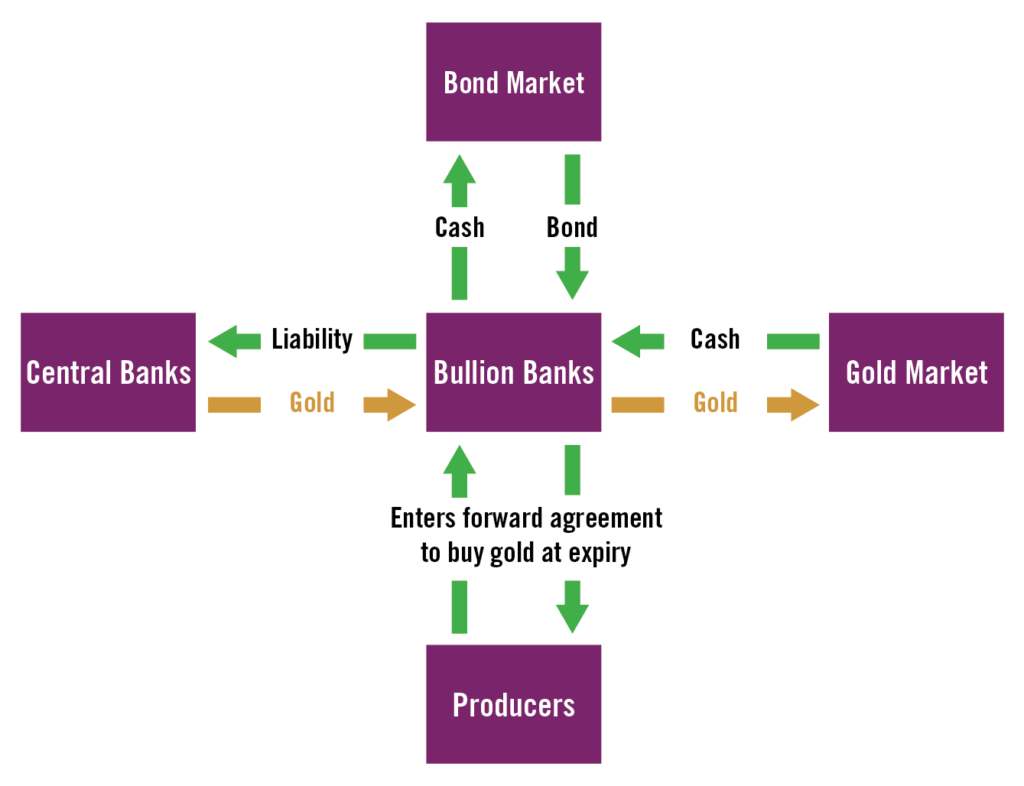

Gold Interest Rate Mechanics

Central banks can generate material yield from gold holdings via uncollateralised loans to a bullion bank. Given that the yellow metal is a monetary asset for central banks, it can be lent out on a term deposit like any other currency in their reserve portfolio. Most commonly, a central bank will place gold on deposit with a bullion bank, in return for a deposit rate. Maturities can vary, but 1-month, 3-month and 12-month tenures are the most common. At maturity, the gold is returned with the interest paid either in gold or fiat.

Deposit rates are derived and set independently by bullion banks. Due to gold’s inherently lower risk (eg. no one’s liability), the yellow metal tends to deliver lower returns than corporate or even government bonds.

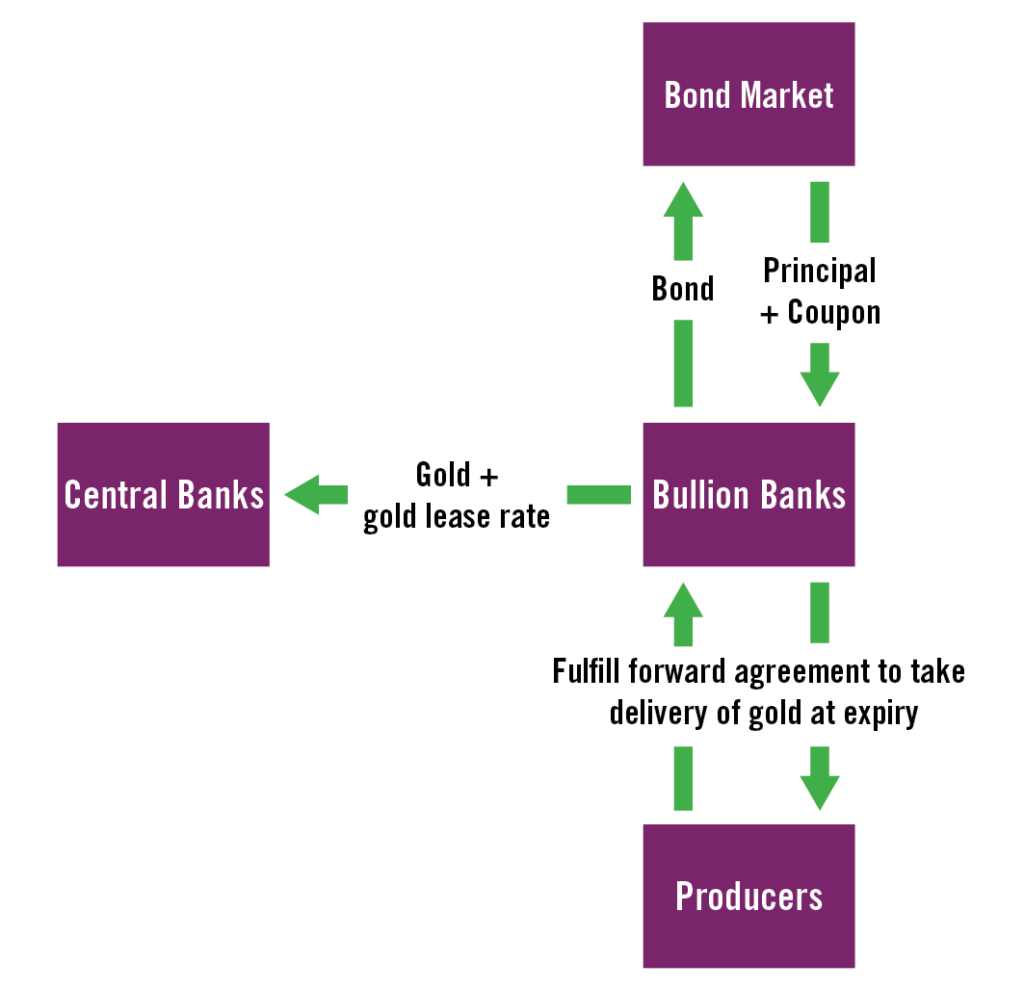

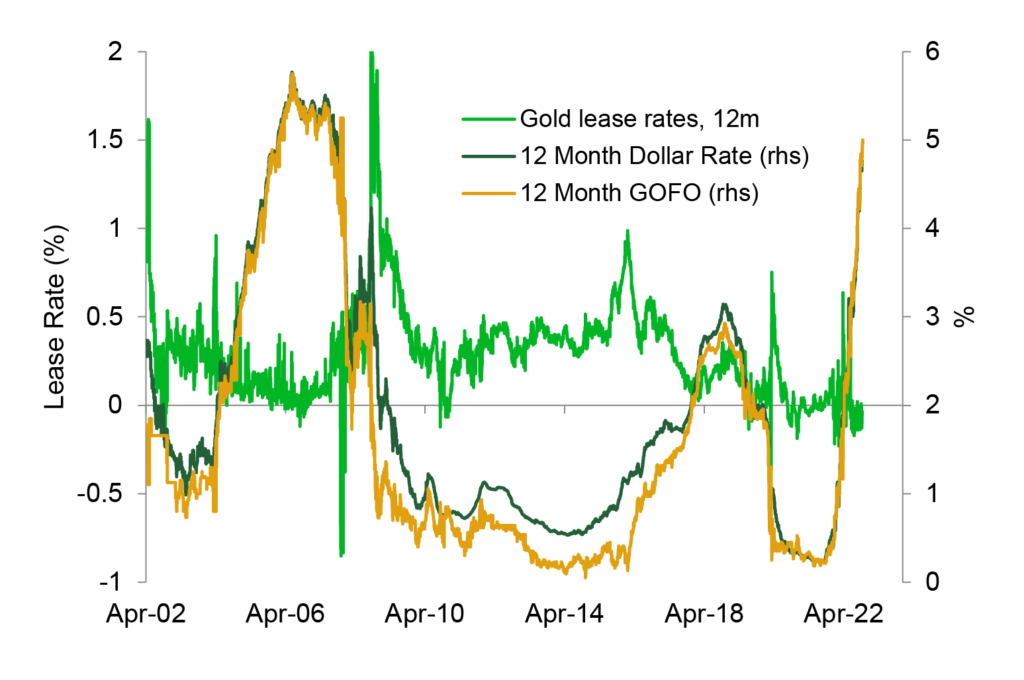

Yield from their gold holdings can also be generated via a gold swap, or more specifically, a repurchase agreement that simulates a swap. In this instance, a central bank sells its gold to a bullion bank with the promise to buy back the gold at a later date. The central bank pays interest equivalent to the GOFO rate (forward swap rate).

In this context, the GOFO rate is akin to a US dollar loan using gold as collateral. Formally, it is defined as the rate at which market-making members of the London Bullion Market Association (LBMA) will lend gold on swap against US dollars. The central bank is then able to reinvest the funds at LIBOR (more recently SOFR) and earn the premium between the dollar rate and GOFO, which amounts to the gold lease rate.

The gold lease rate is typically an over-the-counter instrument, it can be best comprehended through the interaction of the demand and supply of borrowed gold, which will be the focus for the purpose of discussion.

Entering a forward sale agreement

Exiting the forward sale agreement

Decades-High Gold Yields – A Potential Boon For Central Banks

While volatile, we project that the market environment is conducive to delivering consistently higher positive lease rates, which should be quite accretive for central banks willing to deposit metal with a bullion bank in good standing.

The World Gold Council model has shown that real rates, central bank gold holdings of CBGA signatories, producer hedging demand, the real price of gold, the VIX and gold spec positioning explained the 3-month lease rate with a 62% accuracy, with the 12-month rate having an even better 74% success rate. TD Securities analysis has shown similar trends.

| Contemporaneous Regressions: Lease Rate Drivers | ||||||

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 6 | |

| gold returns | -3.537 | 2.448 | 2.235 | |||

| gold vol | -4.779 | -0.368 | -0.806 | |||

| mkt excess return | 0.00883 | 0.0773∗∗∗ | 0.0804∗∗∗ | |||

| smb factor | 0.0119 | 0.0362 | 0.0302 | |||

| hml factor | -0.0138 | 0.0561 | 0.0596 | |||

| 3m Tsy yield | 0.585∗∗∗ | 0.451∗∗∗ | 0.675∗∗∗ | |||

| 10y3m Tsy spread | 0.337∗∗ | -0.0773 | 0.256 | |||

| credit spread (Baa-Aaa) | -1.571∗∗ | -2.471∗∗∗ | -1.695∗∗∗ | |||

| trade-weighted dollar | 11.51∗∗ | 10.23∗∗ | 9.741∗ | |||

| Chicago Fed FCI | 2.121∗∗∗ | -1.993∗∗∗ | -1.991∗∗ | |||

| Money Supply | 20.25 | 3.292 | 20.48 | |||

| VIX | 0.0167 | 0.0839∗∗∗ | 0.0888∗∗∗ | |||

| Bond Illiquidity | 0.562∗∗∗ | 0.611∗∗∗ | 0.677∗∗∗ | |||

| MOVE | 0.0348 | 1.399∗∗ | 0.35 | |||

| Comex Gold stocks g | -1.19 | |||||

| Constant | 0.503 | -1.587 | 1.265∗∗∗ | -1.964∗∗∗ | -5.550∗∗∗ | -6.723∗∗∗ |

| Adjusted R2 | 0.028 | -0.292 | 0.079 | 0.139 | 0.491 | 0.521 |

Source: Risk Premia in Gold Lease Rates, Anh Le and Haoiang Xu; TD Securities

Market Still Has Room For More Hawkish Pricing

Generally speaking, positive price sentiment, a decline in the opportunity cost of holding gold and an aggressive increase in central bank holdings have prompted a fall in producer hedging demand and made the gold carry trade and speculative short-selling less attractive. Factors that are price positive have typically reduced borrowing demand, which depresses gold lease rates.

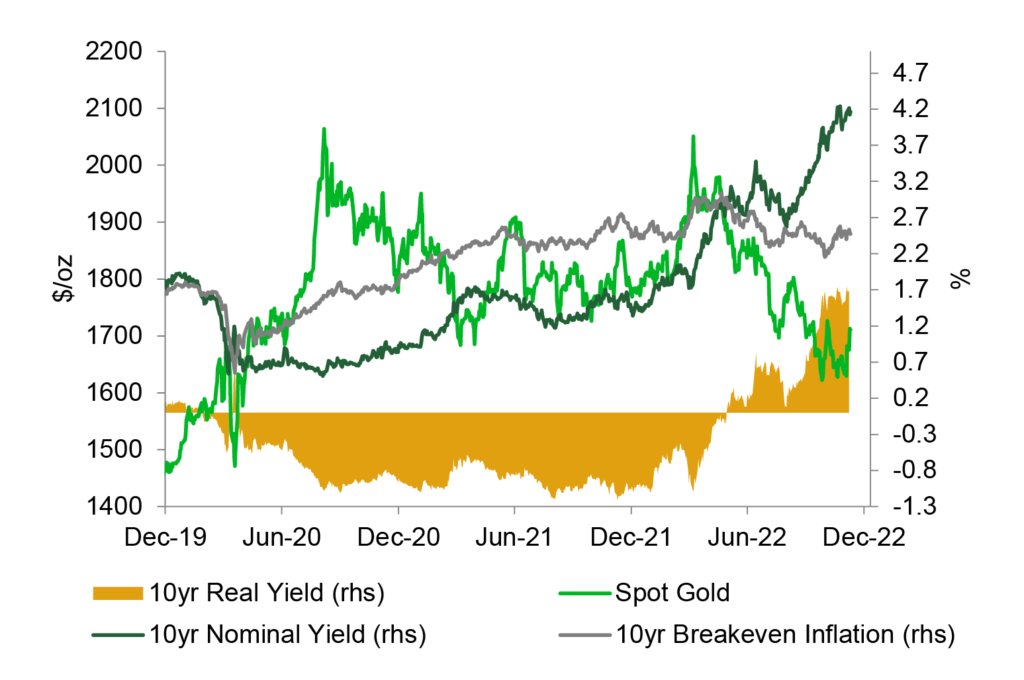

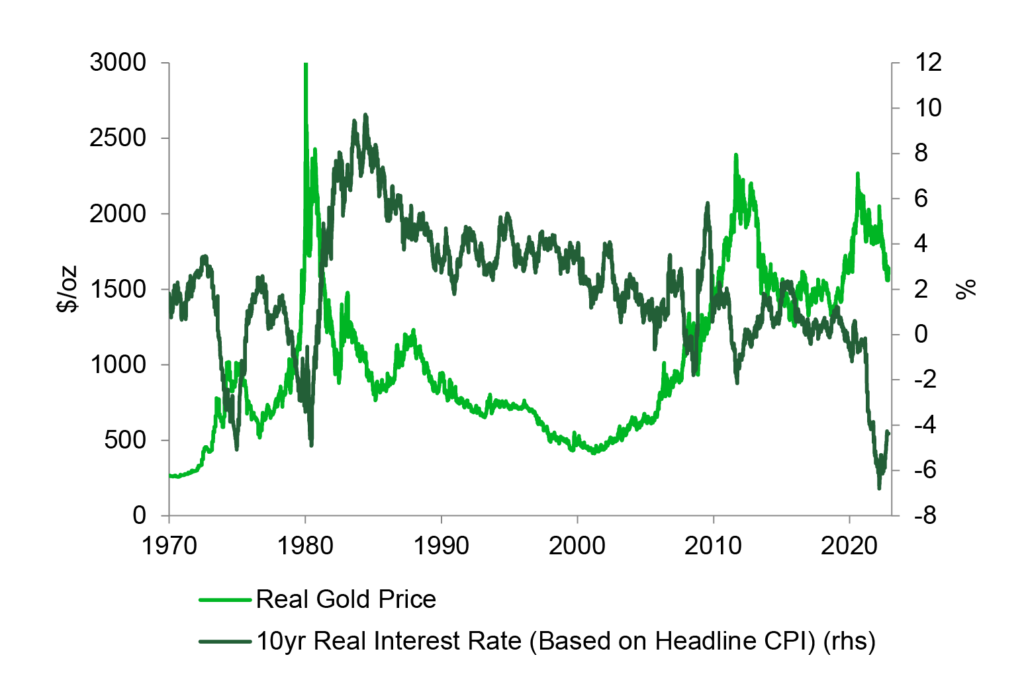

We judge that extremely low central bank interest rates (Fed Funds, other CB policy rates) in the aftermath of the financial crisis, and more recently the COVID pandemic, are a key reason why lease rates were very low between 2010 and 2020. But as real rates across the short end of the Treasury yield curve turn sharply positive and volatility trends higher due to quantitative tightening, sharply higher policy rates and moderating inflation, the conditions which drove lease rates lower will increasingly reverse.

After an outsized 400 tonnes worth of central bank gold purchases in Q3 2022, the official sector purchases are likely to slow relative to the previous pace of accumulation, which should be an additional marginal factor driving gold lease rates above the recent range between 50-75 bps into 2023.

Being Ready Can Be Profitable

Between 1989 and 1999, the gold deposit rate offered a robust source of return for central banks, with the 12-month gold lease rate averaging a hefty 140–200 bps. Since then, however, the rate has fallen sharply, averaging just 54 bps between 2000 and 2009, and we calculate a 15 bps rate between 2010 and 2020.

During the 1980s and 1990s, central banks were aggressive sellers of bullion. As this happened, demand for borrowed gold was increasing at the same time, with many Western European central banks also extending their use of lending, swaps and other derivative instruments. An increase in lending typically resulted in additional gold being sold amid the central bank uncertainty, adding supplies to the market.

The resulting prolonged bear market also prompted miners to take out hedges with bullion banks, helping to create an environment where gold lease rates were elevated and volatile.

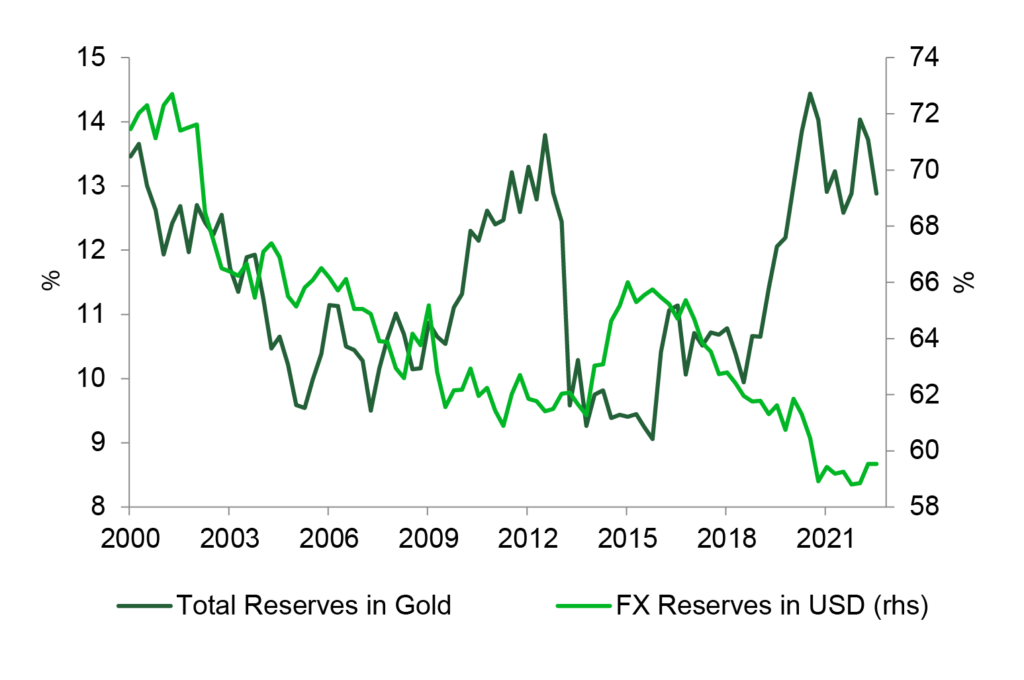

Dollar Debasement Fears Kept CB Holdings Elevated, But Global Slowdown May See a Reversal into 2023

History Shows Gold Lease Rates Can Be Volatile

Different Dynamics Can Drive Lease Rate Changes

Lease Rates Tend to Rise When Precious Metal Sentiment Sours

But even during this period (2000–21), when the monetary policy and macroeconomic environment were negative for gold interest rates, various one-off liquidity crises events such as the great recession and the COVID pandemic shocks and aftershocks generated brief periods when lease rates rose sharply higher, as these shocks precipitated a large need for US dollar liquidity. Banks and corporations sought to use borrowed gold to raise US dollars, which contributed to spikes in gold lease rates. These were opportunities to use gold reserves to generate generous returns, even when the overall environment was not friendly for these types of trades.

The past suggests that there is even more of a case to be made for lease rate spikes in the current environment. As rates rise and central bank balance sheets are drained, liquidity problems are likely to arise periodically, which could spike lease rates. As such, central bank reserve portfolio managers would be prudent to have all their legal document ducks in the row, so they can capitalise on yield spikes should they occur.

Gold Yields Looking Up

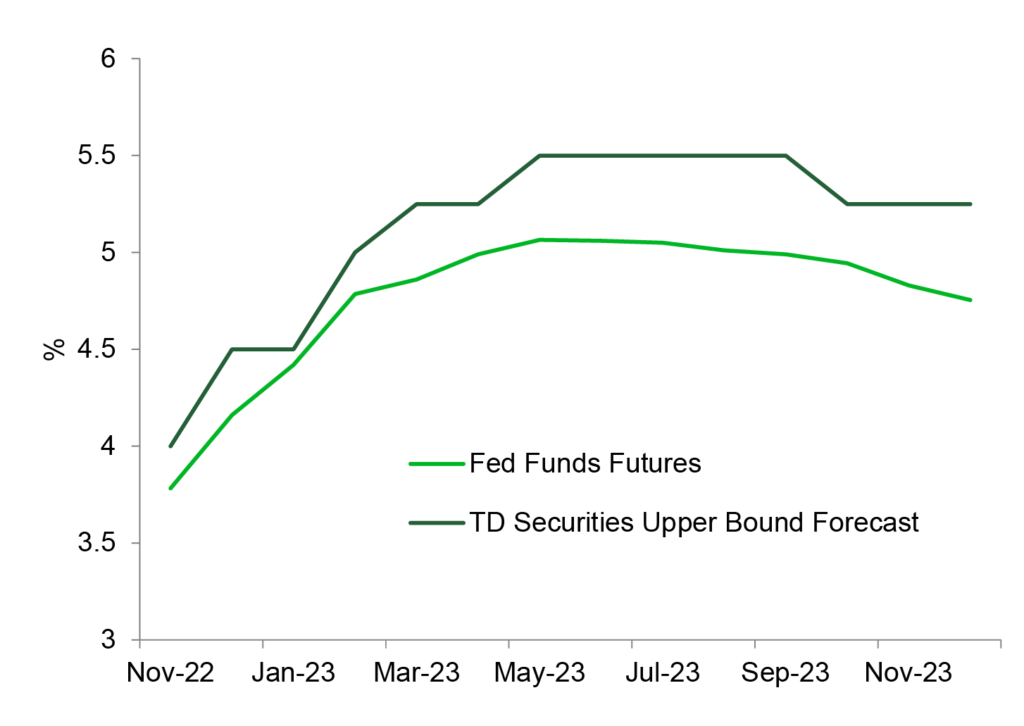

With inflation still raging, the Fed may have no choice but to stick to a hawkish policy stance for a while yet. TD Securities believes that the Fed Funds yield will hit 5.5% and there will be no dovish pivot until late 2023. Conversely, TD Securities judges there will be a general lack of investor interest in gold well into 2023 (as per example: Q3 2022 investment demand, excluding OTC, was down 47% y/y), as the Fed pushed the Fed Funds rate toward 5.50%.

The unwinding of record-setting post-COVID central bank balance sheets, sharply higher equity market volatility and the exit of speculative investors, have already forced non-commercial players (CTAs and other specs) out of all of their long positions, driving prices sharply lower. This helped to lift lease rates up to current fairly high levels, from extreme lows before the tightening.

Aggressive monetary policy tightening has already increased nominal interest rates sharply and reduced inflation expectations, which forced real rates (a key driver of gold) up sharply along the front end, in turn weighing on gold prices. Less investor interest prompted the GOFO rates to lag Treasury yields, pushing lease rates higher. As this trend will continue, particularly on the short end, gold yields also look to be well supported into 2023. This should be exacerbated if physical holders and producers decide to perform some hedging.

Outsized Inflation, Higher Interest Set to Drive Dollar funding and Elevate Lease Rates

Restrictive Monetary Policy Set to Moderate Inflation, Lift Real Rates—a Positive for Gold Deposit Yields

Still, large long positions are being held by family offices and proprietary trading shops. Capitulation from these positions suggests there can be more upward pressure on gold lease rates owing to the potential for further downside price risk and higher carry.

Note

1 BCG & ADDX, Relevance of On-Chain Asset Tokenisation in ‘Crypto Winter’, 2022.

BART MELEK has over 20 years’ experience analysing precious metals, base metals, energy, financial markets, as well as key economies. He has worked closely with commodity, equity and FX trading desks around the world, and has several forecasting distinctions and top global rankings. Bart contributes to the TD Securities strategic view on commodity, various other markets and macroeconomics. Bart is also a sought-after media commentator. Previous to joining TD, he had senior roles in equities, commodities and risk. He holds a master’s degree in economics from York University in Toronto, with an International Finance/Banking Specialization.