Navigate

Article List

- Gold Kilobar Premiums in Asia Trend Upwards

By Koh Guan Ho & Lee Liang Le, Analysts, Kallanish Index Services

- The Dragon & The Merlion: Collaborative Tale of Gold Guardianship

By Nuttapong (Golf) Hirunyasiri, CEO, MTS Gold Group

- My Journey With SBMA and the Singapore Bullion Market

By Martin Huxley, Former Chairman & Current Honorary Advisor, SBMA

- APEX: Leading Derivatives Innovation

By Asia Pacific Exchange

- Navigating the Future: BRINKS Indonesia's Journey of Innovation and Growth

By BRINKS Indonesia

- Gold: a Safe Haven for Private Wealth Investors in Singapore

By Nicolas Mathier, CEO, Global Precious Metals Pte Ltd

- Central Banks Reignite Gold’s Bull Run

By Bart Melek, Managing Director & Global Head of Commodity Strategy, TD Securities

- SBMA News

By SBMA

Article List

- Gold Kilobar Premiums in Asia Trend Upwards

By Koh Guan Ho & Lee Liang Le, Analysts, Kallanish Index Services

- The Dragon & The Merlion: Collaborative Tale of Gold Guardianship

By Nuttapong (Golf) Hirunyasiri, CEO, MTS Gold Group

- My Journey With SBMA and the Singapore Bullion Market

By Martin Huxley, Former Chairman & Current Honorary Advisor, SBMA

- APEX: Leading Derivatives Innovation

By Asia Pacific Exchange

- Navigating the Future: BRINKS Indonesia's Journey of Innovation and Growth

By BRINKS Indonesia

- Gold: a Safe Haven for Private Wealth Investors in Singapore

By Nicolas Mathier, CEO, Global Precious Metals Pte Ltd

- Central Banks Reignite Gold’s Bull Run

By Bart Melek, Managing Director & Global Head of Commodity Strategy, TD Securities

- SBMA News

By SBMA

Central Banks Reignite Gold’s Bull Run

By Bart Melek, Managing Director & Global Head of Commodity Strategy, TD Securities

- The Fed’s dovish pivot, along with another year of very robust official sector buying, are set to feed a gold bull run later in the year. Pending Fed rate cuts in the months to come should prompt traders to grow long exposure. Strong physical demand and official sector buying are projected to lift prices to an average of $2,250/oz next quarter. We expect gold to average $2,113/oz for all of 2024.

- Since discretionary traders and other investors are under-positioned in the yellow metal, an increase in long speculative interest and ETF demand as rates drop suggest that the yellow metal could trade well above our projected quarterly high for a time. The trading high could be $2,300+ sometime over the next six months. If a significant short squeeze materialises, which is possible considering the current under-positioning, a temporary move significantly above even those levels could well be on the cards.

- A record pace of central bank physical gold purchases, renewed investor interest to protect against purchasing power erosion, default risks as US debt grows to alarmingly high levels, and sanctions risks associated with geopolitical tensions in the Middle East and Eastern Europe, could all be factors that not only provide price support as they did last year, but augment any spec-driven rally .

Strong Physical Gold Markets Mute High Real Rates

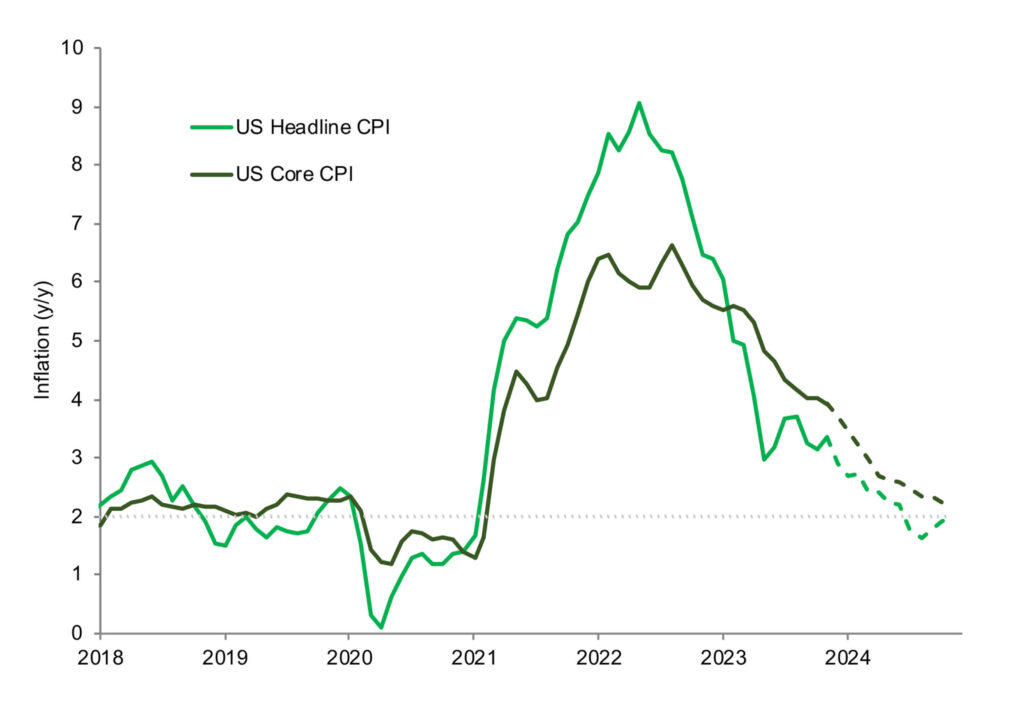

Despite a progressively restrictive monetary policy environment since early-2022, which took interest rates to a two-decade high in the US and across the western world, gold recorded a surprisingly strong performance. It hovered above $2,000+ for a significant part of the last twelve months.

Sharply higher real interest rates along the Treasury curve and a firm USD, which typically spell bad times for the yellow metal, have been offset by strong physical markets. Real interest rates jumped, as policy rates surged, and inflation started to follow a downward trajectory.

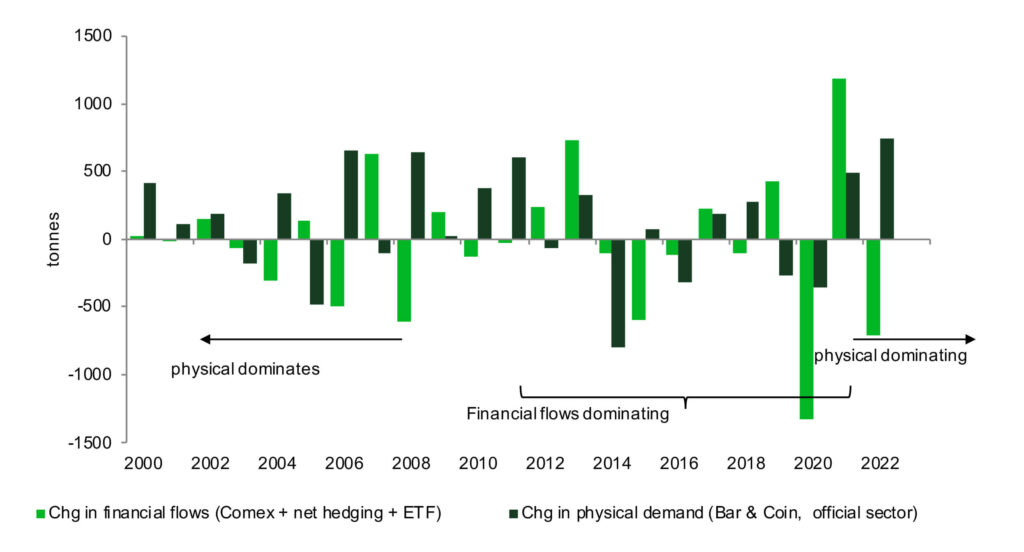

Gold was strong, despite a pronounced speculative investor move away from long exposure and ETF liquidations. Record central bank buying in 2022 and 2023 and Asian investor physical purchases negated the negative impact of high carry costs resulting from the highest interest rate environment in over two decades.

Physical Markets Continue to Dominate Financial Flows

While the yellow metal is well supported in the current trading range above $2,000/oz, there are no compelling reasons why gold should surge in the relative near-term. With US unemployment materially under 4%, wage growth above 4+% y/y, recent monthly jobs gains at 350k+, GDP growth at 3+% and inflation running materially above the implied 2% target, the Fed has little latitude to start to take policy rates down from the current 5.5%.

As such, there is consensus that a March rate cut is off the table and June is being priced. High interest rates, modest speculative appetite, and slumping physical demand suggest that lease rates may move to levels high enough to attract a significant amount of metal into the market. Meanwhile, high carry costs are also likely to see gold being pushed onto the market or may significantly reduce interest in new long acquisitions.

However, we do believe that the US central bank will cut starting by the middle of the year. For a sustained rally to start, the market will need to see a material weakening in economic data and an inflation rate that is closer to 2%. TD Securities expects that rates will drop by some 250 basis points (bps) during the upcoming easing cycle, bringing effective rates to just under 3%. Once this becomes baked into broader expectations, gold should rally again.

Inflation to Remain Above Target Through 24H1- Preventing Imminent Rate Cuts, Gold Bull Run

Positioning, Fed Credibility Angst Are Catalysts for Gold Upside

Lower policy rates are set to send real rates, carry and opportunity costs sharply lower, which should bring speculative and ETF investors back in. This will very much work in tandem with physical markets and relative positioning, which is skewed to the short end, to bring gold above $2,300/ oz later in the year.

US monetary policy authorities have to adhere to the Federal Reserve Act, which mandates that they target both stable inflation and maximum employment at the same time. This suggests that the Fed tends to be tuned to protecting groups in the US against the ravages of inflation and unemployment. The central bank is currently pursuing aggressive restrictive policy because high inflation is hitting households on the lower end of income distribution hard. When the US central bank judges that economic weakness, which no doubt will include elevated unemployment, is hurting the least well off, it is likely to cut policy rates to mitigate the adverse impact on their wellbeing.

The strong likelihood that the Fed will start cutting before inflation reaches the desired level suggests that long-term investors, who have an interest in wealth preservation, may boost portfolio weightings of gold.

Cutting rates significantly before the 2% inflation target is reached may well convince many in the gold market to hedge their long-term purchasing power. They may question the credibility of the Fed’s commitment to the current inflation target. The potential of a US election outcome, which elects politicians who want to cut taxes and grow spending at the same time, may also be a reason investors and central banks continue to buy physical gold.

Official Sector on Gold Binge

Considering that about a quarter of central banks intend to increase their holding this year, we are confident in saying that central bank gold demand will be strong for the foreseeable future. Central banks’ view that the role of the US dollar will be diminished in the years to come will be a big driver of gold demand in the future, as has been outlined in recent surveys that show an increase in this attitude.

In contrast to their views surrounding the greenback, CBs believe that gold’s future role as a reserve asset will grow. Some 62% of them are feel that the yellow metal will have a greater share of total reserves compared to just 46% in the previous sampling. This means continued strong demand from the official sector in the years to come. Last year, this group purchased a near-record 1,037 tonnes and a record 1,082 tonnes in 2022. If central banks’ stated intentions and rate of purchase continue to hold, 2024 should see very strong physical buying.

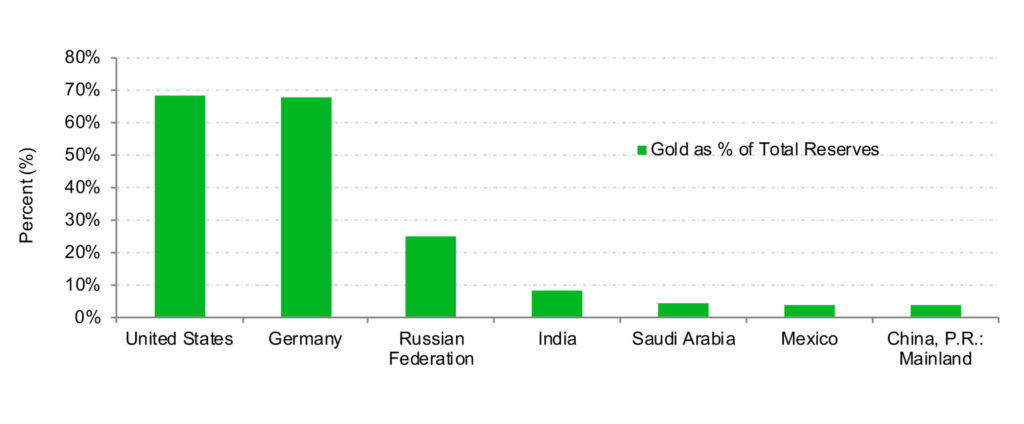

It should be noted that despite China’s recent aggressive buying, the 4.3% gold representation in its FX reserve of $3.2 trillion is still very low. The People’s Bank of China’s (PBoC) gold reserve is much, much smaller than its geopolitical competitors. The US holds some 69.9% of its FX reserve in the form of gold, Germany 69.1%, the Russian Federation 26%, and India 8.8%. If Beijing increased the yellow metal’s FX reserve to just 10%, it would be in the market to buy an additional 2,800+t tonnes at the current price.

Plenty of Room For China to Grow Reserves

BART MELEK has over 20 years’ experience analysing precious metals, base metals, energy, financial markets, as well as key economies. He has worked closely with commodity, equity and FX trading desks around the world, and has several forecasting distinctions and top global rankings. Bart contributes to the TD Securities strategic view on commodity, various other markets and macroeconomics. Bart is also a sought-after media commentator. Before joining TD, he held senior roles in equities, commodities and risk.