Covid-19: Potential Impacts on China’s Economy and Gold Market

By Ray Jia, Research Manager, World Gold Council

Published on March 20, 2020

A Shenzhen jewellery wholesaler’s showroom in February (Image: Showking, Batar Group)

China’s economy is vastly different now compared to 2003, at the height of the SARS outbreak. A consumption-led economy means the economic fallout from the novel coronavirus (Covid-19) outbreak could be larger, argues the World Gold Council’s Ray Jia.

RAY JIA joined the World Gold Council in early 2019, and works within its Market Intelligence Group as a research manager for the China region. He previously held various positions at China Industrial Futures, focusing on market analysis for major commodity classes and international macros for both individual and institutional investors.

This area is for SBMA corporate members only.

To view this content, please log in.

Not yet an SBMA member?

Learn more about SBMA membership here

The Covid-19 outbreak in China is being contained currently as the number of reported infections continues to fall, but China’s economy and gold market is still under pressure.1 To understand the current situation, it helps to look at what has happened in the past – the severe acute respiratory syndrome (SARS) outbreak in 2003 is the closest comparison that can illustrate how Covid-19 may affect China’s economy and gold market. However, one should keep in mind that impacts are not alike since China’s economy is at a different stage now, and the gold market was much smaller then.

SARS SLOWED CHINA’S GDP GROWTH TEMPORARILY

The SARS outbreak, which occurred between March and July 2003, slowed China’s economic growth temporarily.2 China’s gross domestic growth (GDP) growth dropped to 9.1% in Q2 2003, down from 11.1% the quarter before. Growth in key economic indicators during this period, such as retail sales, also took a hit as the streets were left empty as people sought to minimise the spread of the virus.

But the economy soon rebounded: GDP growth in Q3 climbed above 10% as the SARS outbreak was contained. Other key aspects of China’s economy also recovered quickly, supported by:

Structural factors: consumption only accounted for 30% of GDP in 2003 and consumption was hit the hardest by the SARS outbreak.

Cyclical factors: fixed asset investment, including real estate development and equipment investment, was soaring in the early 2000s, fuelling China’s economy.

2003Q2’s GDP growth dipped temporarily

Source: Bloomberg, World Gold Council

Consumption, investment and export’s contribution to GDP in 2003 and 2019

Source: Wind, World Gold Council

CHINA’S ECONOMY: 2003 VS. 2020

China’s economic growth could face more challenges from the Covid-19 outbreak than from SARS in 2003. First, the contribution of consumption to GDP has grown to nearly 60% in 2019, up from 30% in 2003.3 This means a significant hit on consumption will leave a deeper dent on China’s GDP growth. For example, China’s box office revenue during the 2020 Chinese New Year holiday dropped by over 90% from the year before, according to the National Bureau of Statistics.

Second, cyclical supports have lost momentum. Low levels of urbanisation provided large room for China’s property development investment growth in early 2000s. Equipment investment was also on an upward trajectory then as China just joined the World Trade Organization. These factors fuelled China’s economy in 2003, but both measures currently are at different stages due to a stricter housing price stabilisation policy and structural economic transformation.4

Property investment has been an important driver of China’s economy…

Source: Wind, World Gold Council

…so is equipment investment

Source: Wind, World Gold Council

EFFECTS ON THE GOLD JEWELLERY MARKET

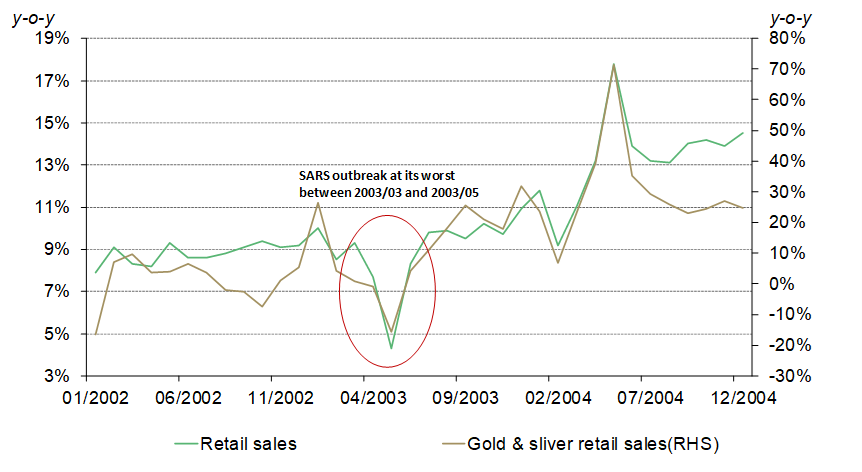

China’s jewellery demand dropped sharply during the SARS outbreak. According to the National Bureau of Statistics, monthly gold and silver products retail sales during the SARS period kept declining. And in Q2 2003, China’s jewellery demand plunged to 41.7 tonnes, a 54% decline from the previous quarter and 21% lower than the same period in 2002, the lowest level in 20 years.

Jewellery retail store during Covid-19 (Image: China Gold Jewellery)

Covid-19 has left China’s jewellery industry in limbo. According to a recent survey by China Gold Association, even though more than 50% of jewellery stores reopened with shorter business hours, very few customers turned up, as the public is avoiding leaving their homes unnecessarily to avoid infection.

With deserted stores comes cash flow issues, but leading brands have taken action. To help their franchisees – representing 90% of jewellery retail stores in China – weather the storm, leading jewellery retailers have lowered or even waived store rental or franchise fees during this critical period.

The supply chain is also under pressure. Our trade partners in Shenzhen, China’s jewellery manufacturing hub, have told us that major manufacturing lines have resumed with strict working arrangements and protection for employees. However, many manufacturing plans are behind schedule, with fewer working days and lower efficiency due to more stringent health protection measures.

New gold jewellery products by a leading retailer (Image: Chow Tai Fook)

The adoption of innovations among jewellers is also likely to accelerate. Upon realising the benefits of bringing businesses online when everyone stays home, jewellers could increase their investment into digital platforms and online retail channels. Meanwhile, online consumers, mainly the younger generation, will become the focus of jewellery retailers, steering their product range towards lighter, more affordable pieces, which are preferred by this demographic in China.

Finally, the gold price’s solid performance in February serves as an excellent example demonstrating gold jewellery’s intrinsic monetary value compared to other products. This will certainly benefit the jewellery industry in the long run.

Gold retail sales were hampered during SARS

Source: National Bureau of Statistics, World Gold Council

Chinese gold price follows international gold price closely

Source: Bloomberg, World Gold Council

CHINA’S GOLD INVESTMENT MARKET

The SARS outbreak’s influence on Chinese local gold price was negligible. In 2003, factors such as US-Iran tensions, the Iraq War, the US dollar and the US Treasury yields were driving the gold price in China. In other words, gold’s performance during the SARS period had a very low correlation with the SARS outbreak that caused sudden shocks to China’s equity market and economy. At the same time, China’s gold investment market was much smaller back then.

While major Chinese assets such as stocks and commodities were hampered by the virus on the first trading day after the Chinese New Year holiday, gold soared. Evident corrections in major assets contributed but more importantly, easing monetary policy environment and rising geopolitical tensions in the Middle East during this period were the major factors lifting international gold prices.

Risk hedging demand and the bullish gold price trend ignited Chinese investors’ passion in gold. The daily trading volume of Au(T+D), the margin-traded gold contract at the Shanghai Gold Exchange, grew by nearly 200% in February. Chinese gold ETF holdings also grew by more than 3 tonnes that month.5 With independent drivers from most domestic assets, gold’s role as an effective risk-diversifying tool for Chinese investors is gaining increasing attention.

However, China’s bar and coin’s offline retail demand could remain subdued in the near term. First, the high gold price might deter some investors. Second, the virus’ potential damage to China’s economy could mean lower purchasing power among consumers. Finally, similar to jewellery sales, bar and coin demand is also vulnerable to empty streets.

Notes

1

Wang Xiaoyu, “Confirmed, suspected cases of novel coronavirus infection declining nationwide”, China Daily, 2 March 2020.

For more information on China’s structural transformation, see: Chi Fulin, “Transformation to quality growth”, China Daily, 11 June 2017 and Shujie Yao, “China faces economic headwinds, but fundamentals remain strong”, China Daily, 26 November 2019.

5

Excluding Bosera’s unlisted funds as they are only updated quarterly.

RAY JIA joined the World Gold Council in early 2019, and works within its Market Intelligence Group as a research manager for the China region. He previously held various positions at China Industrial Futures, focusing on market analysis for major commodity classes and international macros for both individual and institutional investors.

Regional Director, Greater China

MKS PAMP (Singapore) Pte Ltd

Regional Director of Greater China since 2020, and previously Head of Trading. Bernard joined MKS PAMP as a country representative of Singapore in 1996 and moved to Switzerland in 1997. He holds an MBA in International Business from the European University in Geneva. Prior to joining MKS PAMP, Bernard worked 6 years for Standard Chartered Bank in Singapore and Hong Kong as an FX and Bullion Dealer.

Albert Cheng

Chief Executive Officer

Albert Cheng joined the World Gold Council in March 1993 as a Regional Manager, becoming Managing Director, Far East in 2003. He retired at the end of March 2015 and was subsequently named its Advisor. He has also been an International Advisor to the Shanghai Gold Exchange since 2002.

His marketing career began with Dentsu Young & Rubicam, Hong Kong in the early 80’s. He began gold marketing in July 1985 when he joined the Royal Canadian Mint as a Regional Manager for Southeast Asia.

He was appointed honorary CEO of SBMA in November 2015. He is responsible for the success and strategic development of SBMA in partner with the Chairman and the Management Committee. Also, he is responsible for maintaining accountability to and the quality of, the Association’s Membership and the annual Asia Pacific Precious Metals Conference (APPMC) as well as representing the interests of the Association in relation to regulators, investors, media and international precious metal markets, and also responsible for all the legal and regulatory aspects of the work of the Association.

Margaret Wong

BUSINESS DIRECTOR

Margaret Wong, Business Director at SBMA (Singapore Bullion Market Association), brought valuable experience from her previous role at the World Gold Council (WGC). Her tenure at WGC provided her with extensive exposure to the gold community in Singapore and the broader region. This background has been instrumental in establishing strong working relationships within the industry.

Margaret’s role at SBMA encompasses a diverse range of responsibilities. She oversees office management, business support processes, finance, and administrative functions essential for the smooth operation of the team and management committee. Additionally, Margaret handles membership matters, member communications, and addresses public inquiries related to SBMA.

One of Margaret’s key responsibilities is coordinating with the Event Management Company for SBMA’s prestigious annual event, the Asia Pacific Precious Metals Conference. This flagship conference plays a crucial role in the industry, making her involvement pivotal in its success.

Described as resourceful and self-motivated, Margaret Wong brings a wealth of skills and experience to her role at SBMA, ensuring efficient operations and effective engagement within the precious metals community in Singapore and beyond.

Fabian Lew

MARKETING & COMMUNICATIONS OFFICER

Fabian was a Business Development and Marketing Associate before joining SBMA. He graduated from Singapore Management University with a Bachelor’s degree in Economics.

He has joined SBMA since February, 2022.

Ms Crystal Xu

Vice President

TD Securities

Based in Singapore, Crystal has over a decade of experience in the metals market, specializing in trading, structuring, and delivering solutions for institutional and commercial clients across Asia. She leads initiatives spanning both physical and derivative products and plays a central role in advancing TD’s regional metals strategy. With deep expertise in market dynamics and strong cross-functional collaboration, she helps drive business growth, product innovation, and risk-informed decision making across the firm’s Asia-Pacific platform.

Clara Chang

MARKETING & COMMUNICATIONS EXECUTIVE

Clara Chang joins SBMA as the Marketing & Communications Executive, enriching the team with her extensive experience in content creation, social media management, and digital marketing. Prior to joining SBMA, Clara held the position of Marketing Executive at her previous job. She holds two bachelor’s degrees from the University at Buffalo, one in International Trade and another in Geographical Information Science. Her core duties will include maintaining the SBMA website, managing the quarterly Crucible newsletter, among other responsibilities.

Emily Oh

OPERATIONS & ADMIN EXECUTIVE

Emily Oh is the Operations & Admin Executive, a seasoned professional who values teamwork and effective communication. She is skilled at adapting to new challenges and takes a proactive and resourceful approach to every task. Before joining SBMA, Emily had experience coordinating international travel arrangements and spearheading community initiatives. Her role at SBMA will be providing operational and administrative support for projects and other matters to the team.

Lee Jia Yi

OPERATIONS & ADMIN EXECUTIVE

Before joining SBMA, Jia Yi worked as an Admin & Reporting Officer in her previous role. She holds a Diploma in Business & Social Enterprise from Ngee Ann Polytechnic. Jia Yi is responsible for managing and maintaining physical and digital files in SBMA, supporting invoicing processes, reconciling receivables and payables, coordinating meetings and conferences. Additionally, she will provide support to the team and assist the Business Director in managing the Association’s office operations and general administrative activities.

Ms Pawan Nawawattanasub

CEO

YLG Bullion Singapore Pte Ltd

Pawan is the CEO of YLG Bullion Singapore and founder of YLG Bullion International. She has almost 40 years of experience in the jewellery industry and established YLG in Thailand in 2003. In 2012, she brought YLG to Singapore. She sits on the Board of Directors of the Thailand Gold Traders Association, the Thailand Futures Exchange’s Arbitration Committee, and the Rotary Bangkok committee. She holds a master’s degree in Political Science.

Mr Shaokai Fan

Head of Asia-Pacific (ex China) and Global Head of Central Banks

World Gold Council

Shaokai Fan is the Global Head of Central Banks at the World Gold Council, responsible for advising governments on gold matters, and enhancing the gold market through engagement, dialogue, and thought leadership. He works directly with central banks and sovereign wealth funds on investment considerations. Prior to this position, Shaokai held multiple roles at Standard Chartered Bank, including Director for Asia Strategic Initiatives and Associate-Director for Public Sector coverage. Shaokai holds a Masters of Public Administration from Columbia University and the London School of Economics, and an undergraduate degree in finance and economics from New York University.

Mr Alan Liew

Head of Bullion & Commodities Trading

United Overseas Bank Limited

Alan is Head of Bullion and Commodities Trading for Group Trading in Global Markets, United Overseas Bank (UOB). Alan joined UOB and started the bank’s commodities trading business in 2014, previously he spent eight years in Standard Chartered Bank (SCB) trading both precious and base metals. During his tenure at SCB, he obtained the SGE gold trader licence and was part of the pioneering team for the SGE business and the FX quantitative trading team. Prior to trading, he worked for Monetary Authority of Singapore in the Financial Risk Management Division. He holds a BSc (Hon) in Computer Science at National University of Singapore and a MSc in Financial Engineering at Nanyang Technological University.

Mr KL Yap

General Manager, Singapore Refining Business Unit

Metalor Technologies (Singapore) Pte Ltd

KL YAP is the General Manager of Metalor Technologies (Singapore) Pte Ltd’s Singapore Refining Business Unit. He joined Metalor in 2013, initially in Refining Sales. In 2014, he became Refining Business Unit Manager, leading the development of a new precious metal refinery. KL was Vice Chairman of SBMA from 2017 to 2021, now serving as Chairman. With a degree in business commerce, finance, and marketing, he brings prior experience from refinery and heavy industries.

Mr Vinh Nguyen

Head of Precious Metals, Asia

StoneX APAC Pte Ltd

Vinh Nguyen joined StoneX Group in Singapore at the beginning of 2008 and responsible for its APAC precious metals activities since 2019 until now.

Mr Kazuya Naoki

Head of Metals, Asia

ICBC Standard Bank Plc, Singapore Branch

Kazuya (Kaz) Naoki is the Head of Metals, Asia of ICBC Standard Bank in Singapore and is responsible for the precious & base metals sales and trading in the region. He joined Standard Bank Plc Tokyo Branch in 2008 and was relocated to its Singapore Branch in 2013 whose controlling stake was acquired by the Industrial and Commercial Bank of China in 2015. Prior to joining Standard Bank, Kaz spent 11 years focusing on commodity trading and risk management with Mitsui & Co in Tokyo, Sydney and London. Kaz has been serving on the SBMA Management Committee since 2016.

Mr Andrew Clarke

Head of Brink’s Global Services

Brink’s Global Services Pte Ltd

Andrew Clarke is the Head of BGS (Brink’s Global Services) for Singapore, Indonesia, Malaysia and Brunei. He has held various leadership positions throughout his career in secure logistics and risk management with Brink’s, which started in Hong Kong in 2010. Andrew relocated to Singapore in 2018 to expand the precious metals line of business along with Brink’s portfolio of services and industries.

Mr Raman Walia

Executive Director, Head of Commodities Sales – APAC

JP Morgan Chase Bank N.A.

Raman is Executive Director and Head of Commodities Sales, APAC, for J.P. Morgan. He joined JPMorgan in 2008 in New York, moved to Singapore in 2011, and helped expand the precious metals business in the region. Raman has an MBA from Cornell University, and likes to travel in his spare time.

Mr Nuttapong Hirunyasiri

CEO

MTS Gold Global Trading Pte Ltd

Nuttapong Hirunyasiri is the CEO of MTS Gold Group, one of Thailand’s top 10 companies and top 3 bullion companies. He started MTS Gold Group’s first overseas office in Singapore and has been expanding the group business internationally. He focuses on product development and innovation for gold investment, with the aim of being a leader in providing the full suite of gold investment services in the ASEAN region.

Mr Nikos Kavalis

Managing Director

Metals Focus Singapore Pte Ltd

Nikos Kavalis is a founding partner of Metals Focus. He has over 20 years of experience in precious metals, having previously worked for the Royal Bank of Scotland and GFMS. Since September 2019, Nikos has been based in Singapore, where he also runs the local subsidiary of Metals Focus.