This area is for SBMA corporate members only.

To view this content, please log in.

Not yet an SBMA member?

Learn more about SBMA membership here

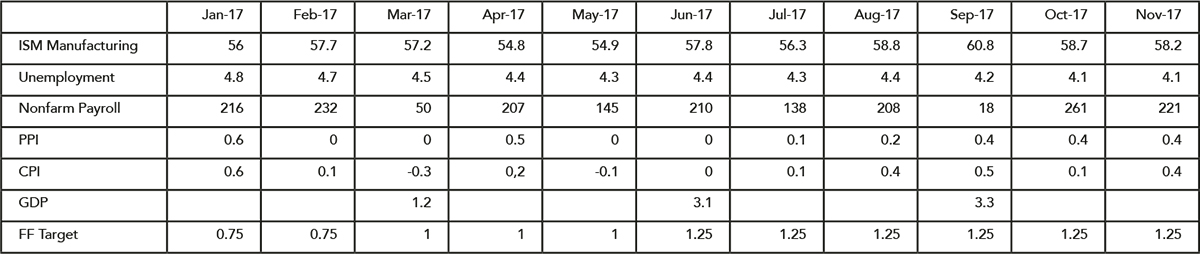

Economic data in 2017 has continued to indicate a moderate global economic recovery. Strong corporate earnings, low unemployment and renewed talk of tax reform optimism in the US is causing investors who missed the stock market rally to chase after higher prices.

On the back of the continued recovery of fundamentals, US and EU central banks have gradually reduced their monetary policy stimulus levels. The Federal Reserve Bank has especially tilted to reduce the size of its balance sheet to reverse the effects of its quantitative easing. There may also be more rate hikes on the cards.

Despite the expectation of continuing rate hikes and a balance sheet reduction, many asset classes performed well in 2017. The S&P 500 has been in the bull channel with a very small dip, and there were no signs of correction. It closed at 2,673 and gained 19.42% in the year to date (29 Dec). Ten-year yields on US Treasury bonds have remained in the range of 2.02–2.62%, closed at 2.40% for the year. Gold has been overshadowed by performance of the equity market, but it has managed to remain in the wide bull channel. The range of the year to date is $1,147–1,357 per ounce, with the closing price at $1,302 – an increase of 13.5% since the end of 2016.

Source: Bloomberg

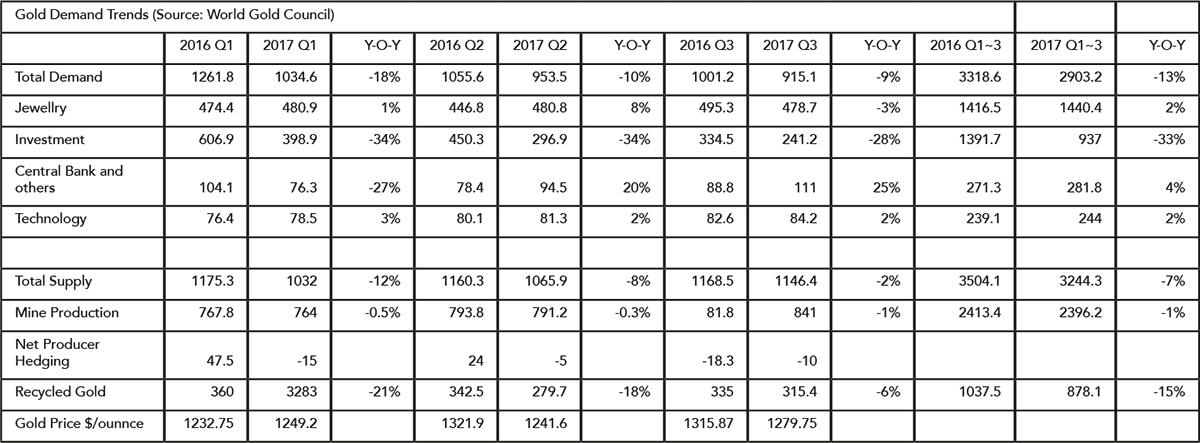

Gold demand trends

Source: Bloomberg

A major driver of the contraction on investment has been gold-backed ETFs. The price of gold has been well supported despite a contraction of demand, but it was not the only preferable asset class for the ETF investors as stock markets have taken centre stage throughout the year.

Monetary policy

The Federal Reserve Bank is expected to continue to keep rate hikes on the cards and its intention may be to raise interest rates to 2.25%. However, the 2/10 yield curve, which peaked at 265bp in December 2013 and flattened to 58bp in December 2017, hints at a recession in the future. Besides, a tapering of the balance sheet may create unexpected shocks in the economy and may also impact asset prices. As such, it will not be an easy for the Federal Reserve Bank to carry on with interest rate hikes and tapering.

It is also expected that any European Central Bank (ECB) interest rate hike and tapering may be few years behind the Federal Reserve Bank. As such, it will be an even more difficult ride for the ECB if it carries on with its policy.

Yield Source: Bloomberg

Economic growth

Economic data has not shown any signs of weakness, and positive fundamental outlook in the United States should maintain overall sentiment towards the economy at least for the first quarter, but concerns over the pace of Federal Reserve Bank action, wage pressures and higher commodity prices may put a dampener on growth. The International Monetary Fund’s GDP outlook for 2018 is Global: 3.7%, US: 2.3%, Germany: 1.8%, and China: 6.5%.

Risk factors

A number of risk factors could affect investment and growth in 2018. Notably, wage pressures in the US, a flat yield curve, the current high valuation of stocks, the fast pace of Federal Reserve Bank interest rate hike and tapering, high commodity prices, instability in North Korea and the Middle East, the deleveraging of assets in China and also US President Trump.

Investment outlook

The long-term prospects for the US dollar, interest rates and stocks have not changed and show no signs of reversal. Despite the extreme actions that have been taken by the Federal Reserve Bank since the Lehman shock, the current recovery has been very moderate compared to recoveries seen in past crises. The Federal Reserve Bank’s rate hike and tapering process may cause an unexpected shock to the economy and investment of assets, but in the meantime, markets remain in a low interest environment with moderate economic growth.

Yield Source: Bloomberg

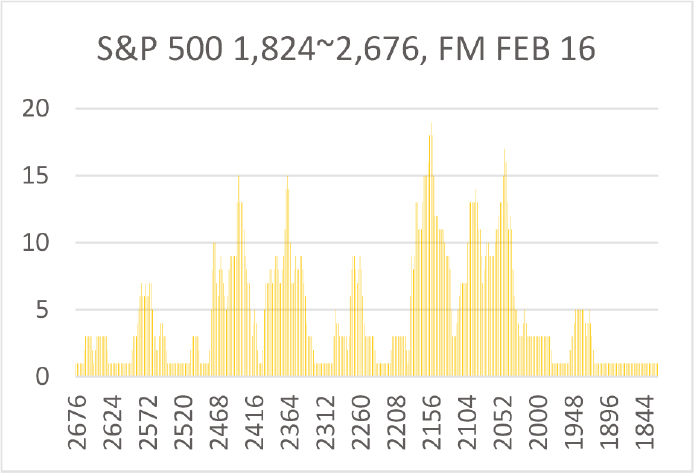

S&P 500: 2,673.61

Higher prices are still attracting buyers and there are no signs of a correction. The chart after the US presidential election (FM Dec 2016) still shows momentum toward 2,684 levels, and 2,908 levels after Bank of Japan’s new policy (FM Feb 2016). Sentiments may therefore be on the long side until market shows signs of reversal from 2,684 or 2,908. It is expected to stay in the 2,366–2,908 range in 2018.

Price Source: Bloomberg

WTI Crude Oil: $60.42

Positions are tilted to the long side and the price is heading towards $64 per barrel. After the test of the $64 level, prices will drop to $46 and will consolidate at this level. However, this scenario is unlikely if oil starts trading below $44, at which point a bear trend is likely. It is expected to hover between $44–64 in 2018.

Price Source: Bloomberg

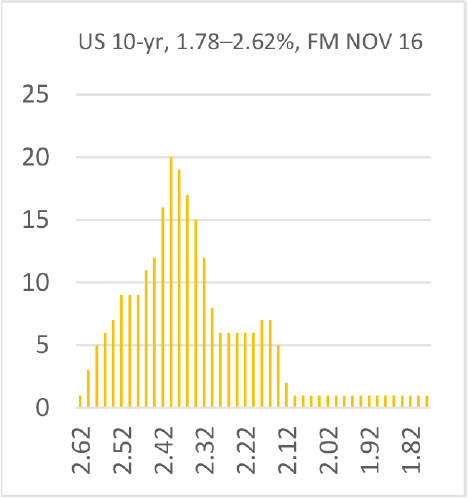

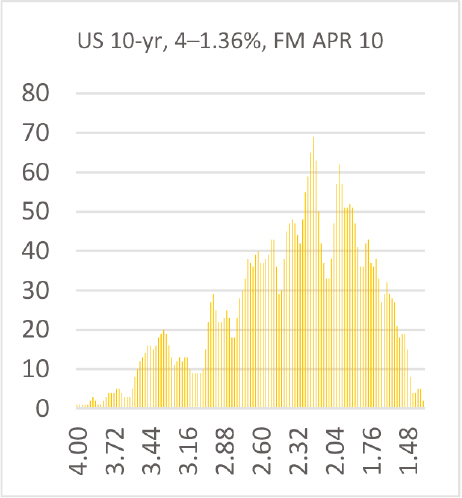

10-Year US Treasury Bonds: 2.405%

Chart since April 2010 still suggests the 10-year yield will reach new lows.

Chart from May 2013 is neutral, but positions are getting neutral to short side.

Chart after US presidential election shows momentum towards 3.02%.

The key levels to watch for the next move are 2.20% and 2.40%. Accepting 2.4% suggests the yield will be heading towards 2.68% and even 3.02%. On the other hand, accepting 2.20% will fix 2.62% as the range high for the year and develop a short squeeze to test below 2%. Under the current fundamentals and the Federal Reserve Bank’s policy, 10-year yields may test 2.68%, but the yield is unlikely to reach 3.02%. Even if 10-year yields reach 3%, the 10-year yield will return to 2.4% and then to 2.2% for a further squeeze as the 2/10 curve hints at a economic slowdown in the future. The range for 2018 is expected to be 1.78–2.68%.

Price Source: Bloomberg

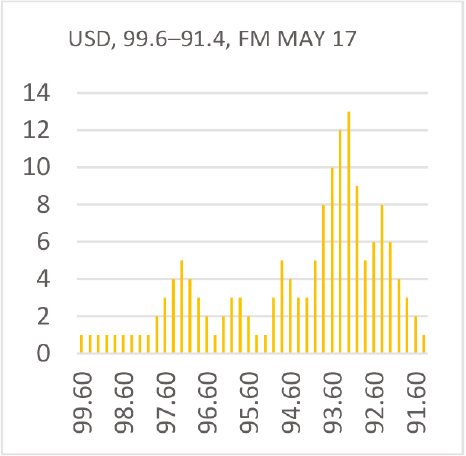

US dollar index: 92.124

The key levels to watch are 95.00 and 91.00. Accepting a value around 95 suggests that the bull run that started in September 2014 is still alive and will be heading to 112.2, while accepting a value below 91 will fix the range high at 103.4 and move towards 86.8 or even lower. The range for 2018 is expected to be 96–85.

Price Source: Bloomberg

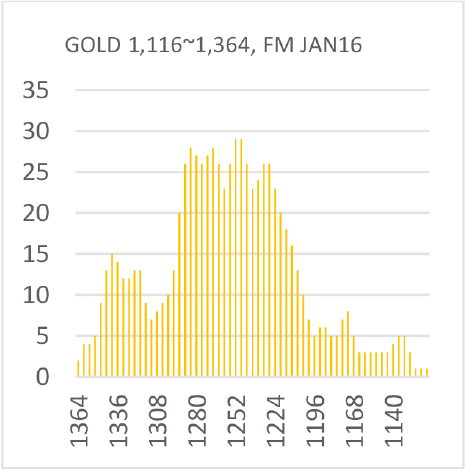

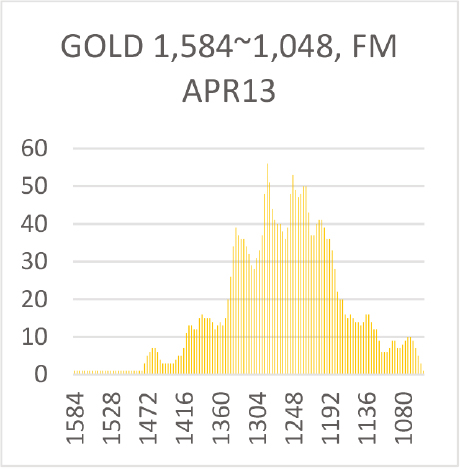

Gold: $1,302.8

Positions still lean towards the short side or are not long enough even for the short term. Price action will be favoured on the long side. The current chart hints at a further squeeze towards $1,380/ounce, then another rally toward to $1,440. This scenario is unlikely if gold starts trading below $1,240. It is expected to remain between $1,240–1,450 in 2018.

Regional Director, Greater China

MKS PAMP (Singapore) Pte Ltd

Regional Director of Greater China since 2020, and previously Head of Trading. Bernard joined MKS PAMP as a country representative of Singapore in 1996 and moved to Switzerland in 1997. He holds an MBA in International Business from the European University in Geneva. Prior to joining MKS PAMP, Bernard worked 6 years for Standard Chartered Bank in Singapore and Hong Kong as an FX and Bullion Dealer.

Albert Cheng

Chief Executive Officer

Albert Cheng joined the World Gold Council in March 1993 as a Regional Manager, becoming Managing Director, Far East in 2003. He retired at the end of March 2015 and was subsequently named its Advisor. He has also been an International Advisor to the Shanghai Gold Exchange since 2002.

His marketing career began with Dentsu Young & Rubicam, Hong Kong in the early 80’s. He began gold marketing in July 1985 when he joined the Royal Canadian Mint as a Regional Manager for Southeast Asia.

He was appointed honorary CEO of SBMA in November 2015. He is responsible for the success and strategic development of SBMA in partner with the Chairman and the Management Committee. Also, he is responsible for maintaining accountability to and the quality of, the Association’s Membership and the annual Asia Pacific Precious Metals Conference (APPMC) as well as representing the interests of the Association in relation to regulators, investors, media and international precious metal markets, and also responsible for all the legal and regulatory aspects of the work of the Association.

Margaret Wong

Executive Director – Head of Operations

Margaret Wong, Executive Director – Head of Operations

at SBMA (Singapore Bullion Market Association), brought valuable experience from her previous role at the World Gold Council (WGC). Her tenure at WGC provided her with extensive exposure to the gold community in Singapore and the broader region. This background has been instrumental in establishing strong working relationships within the industry.

Margaret’s role at SBMA encompasses a diverse range of responsibilities. She oversees office management, business support processes, finance, and administrative functions essential for the smooth operation of the team and management committee. Additionally, Margaret handles membership matters, member communications, and addresses public inquiries related to SBMA.

One of Margaret’s key responsibilities is coordinating with the Event Management Company for SBMA’s prestigious annual event, the Asia Pacific Precious Metals Conference. This flagship conference plays a crucial role in the industry, making her involvement pivotal in its success.

Described as resourceful and self-motivated, Margaret Wong brings a wealth of skills and experience to her role at SBMA, ensuring efficient operations and effective engagement within the precious metals community in Singapore and beyond.

Fabian Lew

MARKETING & COMMUNICATIONS OFFICER

Fabian was a Business Development and Marketing Associate before joining SBMA. He graduated from Singapore Management University with a Bachelor’s degree in Economics.

He has joined SBMA since February, 2022.

Ms Crystal Xu

Vice President

TD Securities

Based in Singapore, Crystal has over a decade of experience in the metals market, specializing in trading, structuring, and delivering solutions for institutional and commercial clients across Asia. She leads initiatives spanning both physical and derivative products and plays a central role in advancing TD’s regional metals strategy. With deep expertise in market dynamics and strong cross-functional collaboration, she helps drive business growth, product innovation, and risk-informed decision making across the firm’s Asia-Pacific platform.

Clara Chang

MARKETING & COMMUNICATIONS EXECUTIVE

Clara Chang joins SBMA as the Marketing & Communications Executive, enriching the team with her extensive experience in content creation, social media management, and digital marketing. Prior to joining SBMA, Clara held the position of Marketing Executive at her previous job. She holds two bachelor’s degrees from the University at Buffalo, one in International Trade and another in Geographical Information Science. Her core duties will include maintaining the SBMA website, managing the quarterly Crucible newsletter, among other responsibilities.

Emily Oh

OPERATIONS & ADMIN EXECUTIVE

Emily Oh is the Operations & Admin Executive, a seasoned professional who values teamwork and effective communication. She is skilled at adapting to new challenges and takes a proactive and resourceful approach to every task. Before joining SBMA, Emily had experience coordinating international travel arrangements and spearheading community initiatives. Her role at SBMA will be providing operational and administrative support for projects and other matters to the team.

Lee Jia Yi

OPERATIONS & ADMIN EXECUTIVE

Before joining SBMA, Jia Yi worked as an Admin & Reporting Officer in her previous role. She holds a Diploma in Business & Social Enterprise from Ngee Ann Polytechnic. Jia Yi is responsible for managing and maintaining physical and digital files in SBMA, supporting invoicing processes, reconciling receivables and payables, coordinating meetings and conferences. Additionally, she will provide support to the team and assist the Business Director in managing the Association’s office operations and general administrative activities.

Ms Pawan Nawawattanasub

CEO

YLG Bullion Singapore Pte Ltd

Pawan is the CEO of YLG Bullion Singapore and founder of YLG Bullion International. She has almost 40 years of experience in the jewellery industry and established YLG in Thailand in 2003. In 2012, she brought YLG to Singapore. She sits on the Board of Directors of the Thailand Gold Traders Association, the Thailand Futures Exchange’s Arbitration Committee, and the Rotary Bangkok committee. She holds a master’s degree in Political Science.

Mr Shaokai Fan

Head of Asia-Pacific (ex China) and Global Head of Central Banks

World Gold Council

Shaokai Fan is the Global Head of Central Banks at the World Gold Council, responsible for advising governments on gold matters, and enhancing the gold market through engagement, dialogue, and thought leadership. He works directly with central banks and sovereign wealth funds on investment considerations. Prior to this position, Shaokai held multiple roles at Standard Chartered Bank, including Director for Asia Strategic Initiatives and Associate-Director for Public Sector coverage. Shaokai holds a Masters of Public Administration from Columbia University and the London School of Economics, and an undergraduate degree in finance and economics from New York University.

Mr Alan Liew

Head of Bullion & Commodities Trading

United Overseas Bank Limited

Alan is Head of Bullion and Commodities Trading for Group Trading in Global Markets, United Overseas Bank (UOB). Alan joined UOB and started the bank’s commodities trading business in 2014, previously he spent eight years in Standard Chartered Bank (SCB) trading both precious and base metals. During his tenure at SCB, he obtained the SGE gold trader licence and was part of the pioneering team for the SGE business and the FX quantitative trading team. Prior to trading, he worked for Monetary Authority of Singapore in the Financial Risk Management Division. He holds a BSc (Hon) in Computer Science at National University of Singapore and a MSc in Financial Engineering at Nanyang Technological University.

Mr KL Yap

General Manager, Singapore Refining Business Unit

Metalor Technologies (Singapore) Pte Ltd

KL YAP is the General Manager of Metalor Technologies (Singapore) Pte Ltd’s Singapore Refining Business Unit. He joined Metalor in 2013, initially in Refining Sales. In 2014, he became Refining Business Unit Manager, leading the development of a new precious metal refinery. KL was Vice Chairman of SBMA from 2017 to 2021, now serving as Chairman. With a degree in business commerce, finance, and marketing, he brings prior experience from refinery and heavy industries.

Mr Vinh Nguyen

Head of Precious Metals, Asia

StoneX APAC Pte Ltd

Vinh Nguyen joined StoneX Group in Singapore at the beginning of 2008 and responsible for its APAC precious metals activities since 2019 until now.

Mr Kazuya Naoki

Managing Director – Head of Metals, Asia ICBC Standard Bank Plc, Singapore Branch

Kazuya (Kaz) Naoki is the Managing Director – Head of Metals, Asia of ICBC Standard Bank in Singapore and is responsible for the precious & base metals sales and trading in the region. He joined Standard Bank Plc Tokyo Branch in 2008 and was relocated to its Singapore Branch in 2013 whose controlling stake was acquired by the Industrial and Commercial Bank of China in 2015. Prior to joining Standard Bank, Kaz spent 11 years focusing on commodity trading and risk management with Mitsui & Co in Tokyo, Sydney and London. Kaz has been serving on the SBMA Management Committee since 2016.

Mr Andrew Clarke

Head of Brink’s Global Services

Brink’s Global Services Pte Ltd

Andrew Clarke is the Head of BGS (Brink’s Global Services) for Singapore, Indonesia, Malaysia and Brunei. He has held various leadership positions throughout his career in secure logistics and risk management with Brink’s, which started in Hong Kong in 2010. Andrew relocated to Singapore in 2018 to expand the precious metals line of business along with Brink’s portfolio of services and industries.

Mr Raman Walia

Managing Director JP Morgan Chase Bank N.A.

Raman is Managing Director for J.P. Morgan. He joined JPMorgan in 2008 in New York, moved to Singapore in 2011, and helped expand the precious metals business in the region. Raman has an MBA from Cornell University, and likes to travel in his spare time.

Mr Nuttapong Hirunyasiri

CEO

MTS Gold Global Trading Pte Ltd

Nuttapong Hirunyasiri is the CEO of MTS Gold Group, one of Thailand’s top 10 companies and top 3 bullion companies. He started MTS Gold Group’s first overseas office in Singapore and has been expanding the group business internationally. He focuses on product development and innovation for gold investment, with the aim of being a leader in providing the full suite of gold investment services in the ASEAN region.

Mr Nikos Kavalis

Managing Director

Metals Focus Singapore Pte Ltd

Nikos Kavalis is a founding partner of Metals Focus. He has over 20 years of experience in precious metals, having previously worked for the Royal Bank of Scotland and GFMS. Since September 2019, Nikos has been based in Singapore, where he also runs the local subsidiary of Metals Focus.